false2021FY0001825079P3M0.45910.43990.4216http://fasb.org/us-gaap/2021-01-31#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2021-01-31#OtherAssetsNoncurrenthttp://www.velo3d.com/20211231#AccruedExpensesAndOtherLiabilitiesCurrenthttp://www.velo3d.com/20211231#AccruedExpensesAndOtherLiabilitiesCurrenthttp://www.velo3d.com/20211231#OtherLiabilitiesAndLeaseLiabilitiesNoncurrenthttp://www.velo3d.com/20211231#OtherLiabilitiesAndLeaseLiabilitiesNoncurrenthttp://www.velo3d.com/20211231#AccruedExpensesAndOtherLiabilitiesCurrenthttp://www.velo3d.com/20211231#AccruedExpensesAndOtherLiabilitiesCurrenthttp://www.velo3d.com/20211231#OtherLiabilitiesAndLeaseLiabilitiesNoncurrenthttp://www.velo3d.com/20211231#OtherLiabilitiesAndLeaseLiabilitiesNoncurrent0.45910.421600018250792021-01-012021-12-310001825079us-gaap:CommonStockMember2021-01-012021-12-310001825079us-gaap:WarrantMember2021-01-012021-12-3100018250792021-06-30iso4217:USD00018250792022-03-21xbrli:shares00018250792021-12-3100018250792020-12-31iso4217:USDxbrli:shares0001825079velo:A3DPrintersMember2021-01-012021-12-310001825079velo:A3DPrintersMember2020-01-012020-12-3100018250792020-01-012020-12-310001825079velo:SupportServicesMember2021-01-012021-12-310001825079velo:SupportServicesMember2020-01-012020-12-310001825079velo:RecurringPaymentMember2021-01-012021-12-310001825079velo:RecurringPaymentMember2020-01-012020-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2020-01-012020-12-310001825079velo:SeriesDRedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:SeriesDRedeemableConvertiblePreferredStockMember2020-01-012020-12-3100018250792019-12-310001825079velo:SeriesARedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:SeriesARedeemableConvertiblePreferredStockMember2020-01-012020-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2020-01-012020-12-310001825079us-gaap:CommonStockMember2019-12-310001825079us-gaap:AdditionalPaidInCapitalMember2019-12-310001825079us-gaap:RetainedEarningsMember2019-12-310001825079us-gaap:CommonStockMember2020-01-012020-12-310001825079us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001825079us-gaap:RetainedEarningsMember2020-01-012020-12-310001825079velo:SeriesDRedeemableConvertiblePreferredStockMemberus-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001825079us-gaap:CommonStockMember2020-12-310001825079us-gaap:AdditionalPaidInCapitalMember2020-12-310001825079us-gaap:RetainedEarningsMember2020-12-310001825079us-gaap:CommonStockMember2021-01-012021-12-310001825079us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001825079us-gaap:RetainedEarningsMember2021-01-012021-12-310001825079us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001825079us-gaap:CommonStockMember2021-12-310001825079us-gaap:AdditionalPaidInCapitalMember2021-12-310001825079us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001825079us-gaap:RetainedEarningsMember2021-12-3100018250792021-09-29xbrli:pure00018250792021-09-292021-09-290001825079us-gaap:BuildingMember2021-06-30utr:sqft0001825079us-gaap:LetterOfCreditMember2021-06-012021-06-300001825079srt:MinimumMembervelo:A3DPrintersMember2021-01-012021-12-310001825079velo:A3DPrintersMembersrt:MaximumMember2021-01-012021-12-310001825079velo:EquipmentOnLeaseMember2021-01-012021-12-310001825079velo:ComputersAndSoftwareMember2021-01-012021-12-310001825079velo:ResearchAndDevelopmentLaboratoryEquipmentMember2021-01-012021-12-310001825079us-gaap:FurnitureAndFixturesMember2021-01-012021-12-310001825079us-gaap:LeaseholdImprovementsMember2021-01-012021-12-310001825079velo:PublicWarrantsMember2021-12-310001825079velo:PrivateWarrantsMember2021-12-310001825079us-gaap:SeriesAPreferredStockMember2021-09-292021-09-290001825079us-gaap:SeriesBPreferredStockMember2021-09-292021-09-290001825079us-gaap:SeriesCPreferredStockMember2021-09-292021-09-290001825079us-gaap:SeriesDPreferredStockMember2021-09-292021-09-290001825079us-gaap:SeriesDPreferredStockMember2021-09-290001825079us-gaap:RedeemableConvertiblePreferredStockMembervelo:LegacyVelo3DMember2021-09-292021-09-290001825079us-gaap:CommonStockMembervelo:LegacyVelo3DMember2021-09-292021-09-290001825079velo:JAWSSpitfireJAWSSpitfireSponsorAndThirdPartyPIPEInvestorsMember2021-09-292021-09-290001825079velo:LegacyVelo3DMember2021-09-292021-09-290001825079velo:JAWSSpitfireAcquisitionCorporationMember2021-09-292021-09-290001825079velo:JAWSSpitfireAcquisitionCorporationMember2021-09-242021-09-240001825079velo:PublicShareholdersMember2021-09-280001825079velo:PublicShareholdersMember2021-09-292021-09-290001825079velo:FounderMember2021-09-292021-09-290001825079velo:LegacyVelo3DMember2021-09-280001825079velo:JAWSSpitfireAcquisitionCorporationMember2020-12-020001825079velo:JAWSSpitfireAcquisitionCorporationMember2021-09-292021-09-290001825079us-gaap:SeriesAPreferredStockMember2021-09-290001825079us-gaap:SeriesBPreferredStockMember2021-09-290001825079us-gaap:SeriesCPreferredStockMember2021-09-290001825079us-gaap:RedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079us-gaap:RedeemableConvertiblePreferredStockMember2020-01-012020-12-310001825079us-gaap:ConvertibleDebtSecuritiesMember2021-01-012021-12-310001825079us-gaap:ConvertibleDebtSecuritiesMember2020-01-012020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-01-012020-12-310001825079velo:WarrantToPurchaseCommonStockMember2021-01-012021-12-310001825079velo:WarrantToPurchaseCommonStockMember2020-01-012020-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001825079us-gaap:EmployeeStockOptionMember2021-01-012021-12-310001825079us-gaap:EmployeeStockOptionMember2020-01-012020-12-310001825079velo:EligibleVelo3DEquityholdersMembervelo:JAWSSpitfireAcquisitionCorporationMembersrt:MaximumMember2021-01-012021-12-310001825079us-gaap:FairValueInputsLevel1Member2021-12-310001825079us-gaap:FairValueInputsLevel2Member2021-12-310001825079us-gaap:FairValueInputsLevel3Member2021-12-310001825079us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001825079us-gaap:FairValueInputsLevel2Memberus-gaap:USTreasurySecuritiesMember2021-12-310001825079us-gaap:FairValueInputsLevel3Memberus-gaap:USTreasurySecuritiesMember2021-12-310001825079us-gaap:USTreasurySecuritiesMember2021-12-310001825079us-gaap:CorporateBondSecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001825079us-gaap:CorporateBondSecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310001825079us-gaap:CorporateBondSecuritiesMemberus-gaap:FairValueInputsLevel3Member2021-12-310001825079us-gaap:CorporateBondSecuritiesMember2021-12-310001825079velo:PublicWarrantsMemberus-gaap:FairValueInputsLevel1Member2021-12-310001825079us-gaap:FairValueInputsLevel2Membervelo:PublicWarrantsMember2021-12-310001825079us-gaap:FairValueInputsLevel3Membervelo:PublicWarrantsMember2021-12-310001825079velo:PrivatePlacementWarrantsMemberus-gaap:FairValueInputsLevel1Member2021-12-310001825079us-gaap:FairValueInputsLevel2Membervelo:PrivatePlacementWarrantsMember2021-12-310001825079us-gaap:FairValueInputsLevel3Membervelo:PrivatePlacementWarrantsMember2021-12-310001825079velo:PrivatePlacementWarrantsMember2021-12-310001825079us-gaap:FairValueInputsLevel1Member2020-12-310001825079us-gaap:FairValueInputsLevel2Member2020-12-310001825079us-gaap:FairValueInputsLevel3Member2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMemberus-gaap:FairValueInputsLevel1Member2020-12-310001825079us-gaap:FairValueInputsLevel2Membervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079us-gaap:FairValueInputsLevel3Membervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembervelo:WarrantLiabilityMember2020-12-310001825079velo:PrivatePlacementWarrantsMembervelo:WarrantLiabilityMember2020-12-310001825079velo:ContingentEarnoutLiabilityMember2020-12-310001825079velo:PrivatePlacementWarrantsMembervelo:WarrantLiabilityMember2021-01-012021-12-310001825079velo:ContingentEarnoutLiabilityMember2021-01-012021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembervelo:WarrantLiabilityMember2021-01-012021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembervelo:WarrantLiabilityMember2021-12-310001825079velo:PrivatePlacementWarrantsMembervelo:WarrantLiabilityMember2021-12-310001825079velo:ContingentEarnoutLiabilityMember2021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembervelo:WarrantLiabilityMember2019-12-310001825079velo:PrivatePlacementWarrantsMembervelo:WarrantLiabilityMember2019-12-310001825079velo:ContingentEarnoutLiabilityMember2019-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembervelo:WarrantLiabilityMember2020-01-012020-12-310001825079velo:PrivatePlacementWarrantsMembervelo:WarrantLiabilityMember2020-01-012020-12-310001825079velo:ContingentEarnoutLiabilityMember2020-01-012020-12-310001825079velo:ComputersAndSoftwareMember2021-12-310001825079velo:ComputersAndSoftwareMember2020-12-310001825079velo:ResearchAndDevelopmentLaboratoryEquipmentMember2021-12-310001825079velo:ResearchAndDevelopmentLaboratoryEquipmentMember2020-12-310001825079us-gaap:FurnitureAndFixturesMember2021-12-310001825079us-gaap:FurnitureAndFixturesMember2020-12-310001825079us-gaap:LeaseholdImprovementsMember2021-12-310001825079us-gaap:LeaseholdImprovementsMember2020-12-310001825079us-gaap:ConstructionInProgressMember2021-12-310001825079us-gaap:ConstructionInProgressMember2020-12-31velo:leased_asset0001825079velo:OfficeAndManufacturingFacilitiesMembervelo:OperatingLeasesExpiringIn2023To2027Member2021-01-012021-12-31velo:lease0001825079velo:OfficeAndManufacturingFacilitiesMembervelo:MonthToMonthOperatingLeaseMember2021-01-012021-12-310001825079velo:OfficeManufacturingAndRDFacilitiesMember2021-01-012021-12-310001825079us-gaap:ManufacturingFacilityMember2021-12-310001825079velo:RDFacilityMember2021-12-310001825079us-gaap:MediumTermNotesMember2021-12-310001825079us-gaap:MediumTermNotesMember2020-12-310001825079us-gaap:LineOfCreditMember2021-12-310001825079us-gaap:LineOfCreditMember2020-12-310001825079velo:PropertyAndEquipmentLoanMember2021-12-310001825079velo:PropertyAndEquipmentLoanMember2020-12-310001825079velo:EquipmentLoanMember2021-12-310001825079velo:EquipmentLoanMember2020-12-310001825079us-gaap:MediumTermNotesMember2019-04-180001825079us-gaap:MediumTermNotesMemberus-gaap:PrimeRateMember2019-04-182019-04-180001825079us-gaap:MediumTermNotesMember2019-04-182019-04-180001825079us-gaap:MediumTermNotesMember2020-12-172020-12-1700018250792021-05-310001825079us-gaap:MediumTermNotesMember2021-05-310001825079us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-05-310001825079velo:EquipmentLoanMember2021-05-310001825079us-gaap:MediumTermNotesMember2021-04-300001825079us-gaap:MediumTermNotesMemberus-gaap:PrimeRateMember2021-05-012021-05-310001825079us-gaap:MediumTermNotesMember2021-05-012021-05-310001825079us-gaap:InterestExpenseMemberus-gaap:MediumTermNotesMember2021-05-012021-05-310001825079us-gaap:MediumTermNotesMember2021-07-012021-07-310001825079us-gaap:MediumTermNotesMember2021-10-292021-10-290001825079us-gaap:MediumTermNotesMember2021-01-012021-12-310001825079us-gaap:MediumTermNotesMember2020-01-012020-12-310001825079us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-08-012021-08-310001825079us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-08-310001825079us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMemberus-gaap:PrimeRateMember2021-08-012021-08-310001825079us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-12-310001825079us-gaap:RevolvingCreditFacilityMember2021-01-012021-12-310001825079velo:PropertyAndEquipmentLoanMember2018-07-020001825079velo:PropertyAndEquipmentLoanMember2018-09-262018-09-260001825079velo:PropertyAndEquipmentLoanMemberus-gaap:PrimeRateMember2018-09-262018-09-260001825079velo:PropertyAndEquipmentLoanMember2020-12-170001825079velo:PropertyAndEquipmentLoanMemberus-gaap:PrimeRateMember2020-12-172020-12-170001825079velo:PropertyAndEquipmentLoanMember2020-12-172020-12-170001825079velo:PropertyAndEquipmentLoanMemberus-gaap:InterestExpenseMember2021-05-012021-05-310001825079velo:PropertyAndEquipmentLoanMember2021-04-300001825079velo:PropertyAndEquipmentLoanMember2021-01-012021-12-310001825079velo:PropertyAndEquipmentLoanMember2020-01-012020-12-310001825079velo:EquipmentLoanMember2020-12-170001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityOneMember2020-12-310001825079velo:EquipmentLoanMember2021-01-012021-12-310001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityOneMember2021-01-012021-12-31velo:advance0001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityOneMember2021-12-310001825079velo:EquipmentLoanFacilityOneMembervelo:SecuredEquipmentLoanFacilityMember2021-12-310001825079velo:SecuredEquipmentLoanFacilityMember2021-12-310001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityTwoMember2020-06-300001825079velo:EquipmentLoanMember2020-06-012020-06-300001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityTwoMember2021-01-012021-12-310001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityTwoMember2020-01-012020-12-310001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityTwoMember2020-12-310001825079velo:EquipmentLoanFacilityTwoMembervelo:EquipmentLoanMember2021-01-012021-12-310001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityTwoMember2021-12-310001825079velo:EquipmentLoanMembervelo:EquipmentLoanFacilityTwoMemberus-gaap:InterestExpenseMember2021-01-012021-12-310001825079velo:ConvertibleNotesDueNovember152024Memberus-gaap:ConvertibleNotesPayableMember2019-11-150001825079velo:ConvertibleNotesDueNovember152024Memberus-gaap:ConvertibleNotesPayableMember2019-12-310001825079velo:ConvertibleNotesDueApril172035Memberus-gaap:ConvertibleNotesPayableMember2020-04-170001825079velo:ConvertibleNotesDueApril172035Memberus-gaap:ConvertibleNotesPayableMember2020-04-172020-04-170001825079velo:ConvertibleNotesDueApril172035Membervelo:SeriesDRedeemableConvertiblePreferredStockMember2020-04-170001825079velo:ConvertibleNotesDueApril172035Memberus-gaap:ConvertibleNotesPayableMember2020-06-112020-06-110001825079velo:ConvertibleNotesDueApril172035Membervelo:SeriesDRedeemableConvertiblePreferredStockMember2020-06-110001825079us-gaap:ConvertibleNotesPayableMembervelo:ConvertibleNotesDueJanuary32023Member2021-01-040001825079us-gaap:ConvertibleNotesPayableMembervelo:ConvertibleNotesDueJanuary32023Member2021-09-012021-09-300001825079us-gaap:ConvertibleNotesPayableMember2020-12-310001825079us-gaap:ConvertibleNotesPayableMember2021-12-310001825079us-gaap:ConvertibleNotesPayableMembervelo:ConvertibleNotesDueJanuary32023Member2021-12-310001825079us-gaap:ConvertibleNotesPayableMembervelo:ConvertibleNotesDueJanuary32023Member2021-09-292021-09-290001825079us-gaap:ConvertibleNotesPayableMembervelo:ConvertibleNotesDueJanuary32023Member2021-01-042021-01-04velo:share0001825079velo:SeriesARedeemableConvertiblePreferredStockMember2020-12-310001825079velo:SeriesBRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:SeriesDRedeemableConvertiblePreferredStockMember2020-12-3100018250792020-04-130001825079velo:SeriesARedeemableConvertiblePreferredStockMember2020-04-132020-04-130001825079velo:SeriesBRedeemableConvertiblePreferredStockMember2020-04-132020-04-130001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2020-04-132020-04-130001825079us-gaap:CommonStockMember2020-04-132020-04-130001825079us-gaap:RedeemableConvertiblePreferredStockMember2020-04-1300018250792020-04-132020-04-130001825079us-gaap:RedeemableConvertiblePreferredStockMember2020-04-132020-04-130001825079us-gaap:AdditionalPaidInCapitalMember2020-04-132020-04-130001825079us-gaap:RetainedEarningsMember2020-04-132020-04-130001825079velo:SeriesDRedeemableConvertiblePreferredStockMember2020-04-132020-04-130001825079us-gaap:RedeemableConvertiblePreferredStockMember2021-12-310001825079us-gaap:RedeemableConvertiblePreferredStockMember2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:WarrantToPurchaseCommonStockMember2021-12-310001825079velo:WarrantToPurchaseCommonStockMember2020-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2021-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2020-12-310001825079us-gaap:EmployeeStockOptionMember2021-12-310001825079us-gaap:EmployeeStockOptionMember2020-12-310001825079us-gaap:StockCompensationPlanMembervelo:A2014StockOptionPlanMember2021-12-310001825079us-gaap:StockCompensationPlanMembervelo:A2014StockOptionPlanMember2020-12-310001825079us-gaap:StockCompensationPlanMembervelo:A2021StockOptionPlanMember2021-12-310001825079us-gaap:StockCompensationPlanMembervelo:A2021StockOptionPlanMember2020-12-310001825079us-gaap:EmployeeStockMember2021-12-310001825079us-gaap:EmployeeStockMember2020-12-310001825079velo:WarrantToPurchaseCommonStockMember2021-12-310001825079velo:WarrantToPurchaseCommonStockMember2020-12-31iso4217:USDvelo:warrant0001825079velo:CommonStockWarrantsDueDecember22025Member2020-12-310001825079velo:CommonStockWarrantsDueJuly22028Member2020-12-310001825079velo:CommonStockWarrantsDueDecember172030Member2020-12-310001825079velo:MeasurementInputExpectedVolatilityMembervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMemberus-gaap:MeasurementInputRiskFreeInterestRateMember2020-12-310001825079velo:PrivatePlacementWarrantsMember2020-12-020001825079velo:PublicWarrantsMember2020-12-020001825079velo:CommonStockWarrantsMember2020-12-310001825079velo:CommonStockWarrantsMember2021-01-012021-12-310001825079velo:CommonStockWarrantsMember2021-12-310001825079us-gaap:MeasurementInputSharePriceMembervelo:CommonStockWarrantsMember2021-12-31velo:alternative_energy_credit0001825079velo:MeasurementInputExpectedVolatilityMembervelo:CommonStockWarrantsMember2021-12-310001825079velo:CommonStockWarrantsMemberus-gaap:MeasurementInputRiskFreeInterestRateMember2021-12-310001825079us-gaap:MeasurementInputExpectedDividendRateMembervelo:CommonStockWarrantsMember2021-12-310001825079velo:SeriesARedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-01-012020-12-310001825079velo:SeriesARedeemableConvertiblePreferredStockMember2020-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2020-12-310001825079us-gaap:RedeemableConvertiblePreferredStockMember2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2019-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2021-01-012021-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2021-12-310001825079srt:MinimumMembervelo:MeasurementInputExpectedVolatilityMembervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:MeasurementInputExpectedVolatilityMembervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembersrt:MaximumMember2020-12-310001825079srt:MinimumMembervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMemberus-gaap:MeasurementInputRiskFreeInterestRateMember2020-12-310001825079velo:WarrantToPurchaseRedeemableConvertiblePreferredStockMembersrt:MaximumMemberus-gaap:MeasurementInputRiskFreeInterestRateMember2020-12-310001825079us-gaap:MeasurementInputExpectedDividendRateMembervelo:WarrantToPurchaseRedeemableConvertiblePreferredStockMember2020-12-310001825079velo:EligibleVelo3DEquityholdersMembervelo:WarrantRedemptionScenarioOneMember2021-09-290001825079velo:EligibleVelo3DEquityholdersMembervelo:WarrantRedemptionScenarioOneMember2021-09-292021-09-290001825079velo:EligibleVelo3DEquityholdersMembervelo:ContingentEarnoutLiabilityScenarioTwoMember2021-09-290001825079velo:EligibleVelo3DEquityholdersMembervelo:ContingentEarnoutLiabilityScenarioTwoMember2021-09-292021-09-290001825079velo:EligibleVelo3DEquityholdersMember2021-09-292021-09-290001825079velo:EligibleVelo3DEquityholdersMembervelo:JAWSSpitfireAcquisitionCorporationMembersrt:MaximumMember2021-09-292021-09-29velo:tranche0001825079velo:EligibleVelo3DEquityholdersMembervelo:JAWSSpitfireAcquisitionCorporationMember2021-09-292021-09-290001825079velo:JAWSSpitfireAcquisitionCorporationMember2021-09-290001825079us-gaap:MeasurementInputSharePriceMember2021-12-310001825079us-gaap:MeasurementInputSharePriceMember2021-09-290001825079velo:MeasurementInputExpectedVolatilityMember2021-12-310001825079velo:MeasurementInputExpectedVolatilityMember2021-09-290001825079us-gaap:MeasurementInputRiskFreeInterestRateMember2021-12-310001825079us-gaap:MeasurementInputRiskFreeInterestRateMember2021-09-290001825079us-gaap:MeasurementInputExpectedDividendRateMember2021-12-310001825079us-gaap:MeasurementInputExpectedDividendRateMember2021-09-290001825079velo:SeriesARedeemableConvertiblePreferredStockMember2021-12-310001825079velo:SeriesCRedeemableConvertiblePreferredStockMember2021-12-310001825079velo:A2014StockOptionPlanMember2020-12-310001825079velo:A2014StockOptionPlanMember2021-01-012021-12-310001825079velo:A2021EquityIncentivePlanMember2021-12-310001825079srt:MinimumMember2021-01-012021-12-3100018250792019-01-012019-12-310001825079us-gaap:EmployeeStockOptionMember2021-12-310001825079us-gaap:EmployeeStockOptionMember2021-01-012021-12-310001825079us-gaap:EmployeeStockOptionMember2020-01-012020-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2020-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2021-12-310001825079us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001825079velo:EarnoutShareUnitsMember2021-01-012021-12-310001825079velo:EarnoutShareUnitsMember2020-01-012020-12-310001825079us-gaap:ResearchAndDevelopmentExpenseMember2021-01-012021-12-310001825079us-gaap:ResearchAndDevelopmentExpenseMember2020-01-012020-12-310001825079us-gaap:SellingAndMarketingExpenseMember2021-01-012021-12-310001825079us-gaap:SellingAndMarketingExpenseMember2020-01-012020-12-310001825079us-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310001825079us-gaap:GeneralAndAdministrativeExpenseMember2020-01-012020-12-310001825079us-gaap:DomesticCountryMember2021-12-310001825079us-gaap:StateAndLocalJurisdictionMember2021-12-310001825079us-gaap:DomesticCountryMember2020-12-310001825079us-gaap:StateAndLocalJurisdictionMember2020-12-310001825079us-gaap:ResearchMemberus-gaap:DomesticCountryMember2021-12-310001825079us-gaap:ResearchMemberus-gaap:StateAndLocalJurisdictionMember2021-12-310001825079us-gaap:ForeignCountryMember2020-12-310001825079us-gaap:ForeignCountryMember2021-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer1Member2021-01-012021-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer1Member2020-01-012020-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer1Member2021-01-012021-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer1Member2020-01-012020-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer2Member2021-01-012021-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer3Member2021-01-012021-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer3Member2021-01-012021-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer3Member2020-01-012020-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer4Member2021-01-012021-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer4Member2020-01-012020-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer4Member2020-01-012020-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer5Member2020-01-012020-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer5Member2021-01-012021-12-310001825079us-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMembervelo:Customer5Member2020-01-012020-12-310001825079us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMembervelo:Customer6Member2020-01-012020-12-310001825079velo:OtherLocationsMembervelo:EquipmentOnLeaseMember2021-12-31velo:assets0001825079country:US2021-01-012021-12-310001825079country:US2020-01-012020-12-310001825079velo:OtherLocationsMember2021-01-012021-12-310001825079velo:OtherLocationsMember2020-01-012020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________ FORM 10-K

_____________________________

| | | | | |

| (Mark One) |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2021

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-39757

______________________________

Velo3D, Inc.

______________________________

(Exact name of registrant as specified in its charter) | | | | | | | | |

| Delaware | 98-1556965 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 511 Division Street, | 95008 |

| Campbell, | California | |

| (Address of Principal Executive Offices) | | (Zip Code) |

(408) 610-3915

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common stock, par value $0.00001 per share | VLD | New York Stock Exchange |

| Warrants to purchase one share of common stock, each at an exercise price of $11.50 per share | VLD WS | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | | Smaller reporting company | ☒ |

| | | Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The aggregate market value of the voting and non-voting stock held by non-affiliates of JAWS Spitfire Acquisition Corporation (“JAWS Spitfire”), our predecessor, on June 30, 2021, the last business day of the registrant's most recently completed second fiscal quarter, based on the closing price of $9.97 for shares of JAWS Spitfire’s Class A ordinary shares then listed on the New York Stock Exchange, was approximately $131.0 million. Ordinary shares beneficially owned by each executive officer, director and holder of more than 10% of ordinary shares have been excluded in that such persons may be deemed to be affiliates.

As of March 21, 2022, there were 183,557,946 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2022 Annual Meeting of Stockholders, or Proxy Statement, to be filed within 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K, are incorporated by reference in Part III. Except with respect to information specifically incorporated by reference in this Annual Report, the Proxy Statement shall not be deemed to be filed as part hereof.

TABLE OF CONTENTS | | | | | | | | |

| | Page |

| | |

| |

| | |

| PART I | | |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| PART II | | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | |

| PART III | | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| PART IV | | |

| | |

| Item 15. | | |

| Item 16. | | |

| | |

| | |

Explanatory Note – Certain Defined Terms

Unless otherwise stated in this Annual Report or the context otherwise requires, references to:

“Board” or “Board of Directors” means the board of directors of the Company.

“Bylaws” means the restated bylaws of the Company.

“Business Combination Agreement” means that certain Business Combination Agreement, dated as of March 22, 2021, by and among JAWS Spitfire, Merger Sub and Legacy Velo3D, as amended by Amendment #1 to Business Combination Agreement dated as of July 20, 2021.

“Certificate of Incorporation” means the restated certificate of incorporation of the Company.

“common stock” means the shares of common stock, par value $0.00001 per share, of the Company.

“Class A ordinary shares” means the Class A ordinary shares, par value $0.0001 per share, of JAWS Spitfire, prior to the Domestication, which automatically converted, on a one-for-one basis, into shares of common stock in connection with the Closing.

“Class B ordinary shares” means the Class B ordinary shares, par value $0.0001 per share, of JAWS Spitfire, prior to the Domestication, which automatically converted, on a one-for-one basis, into shares of common stock in connection with the Closing.

“Closing” means the closing of the Merger.

“Closing Date” means September 29, 2021.

“Code” means the Internal Revenue Code of 1986, as amended.

“Domestication” means the domestication contemplated by the Business Combination Agreement, whereby JAWS Spitfire effected a deregistration and a transfer by way of continuation from the Cayman Islands to the State of Delaware, pursuant to which JAWS Spitfire’s jurisdiction of incorporation was changed from the Cayman Islands to the State of Delaware.

“DGCL” means the General Corporation Law of the State of Delaware.

“Earnout Shares” means up to 21,758,148 shares of our common stock issuable pursuant to the Business Combination Agreement to certain Legacy Velo3D equity holders upon the achievement of certain vesting conditions.

“Equity Incentive Plan” means the Velo3D, Inc. 2021 Equity Incentive Plan.

“ESPP” means the Velo3D, Inc. 2021 Employee Stock Purchase Plan.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Founder Shares” means the 8,625,000 shares of our common stock issued to the Sponsor and the other Initial Stockholders in connection with the automatic conversion of the Class B ordinary shares in connection with the Closing.

“GAAP” means United States generally accepted accounting principles.

“Initial Stockholders” means the Sponsor together with Andy Appelbaum, Mark Vallely and Serena J. Williams.

“IPO” means the Company’s initial public offering, consummated on December 7, 2020, of 34,500,000 units (including 4,500,000 units that were issued to the underwriters in connection with the exercise in full of their over-allotment option) at $10.00 per unit.

“JAWS Spitfire” refers to JAWS Spitfire Acquisition Corporation, a Cayman Islands exempted company, prior to the Closing.

“Legacy Velo3D” means Velo3D, Inc., a Delaware corporation (n/k/a Velo3D US, Inc.), prior to the Closing.

“Legacy Velo3D equity holder” means certain former stockholders and equity award holders of Legacy Velo3D.

“Merger” and “Reverse Recapitalization” mean the merger contemplated by the Business Combination Agreement, whereby Merger Sub merged with and into Legacy Velo3D, with Legacy Velo3D surviving the merger as a wholly-owned subsidiary of the Company on the Closing Date.

“Merger Sub” means Spitfire Merger Sub, Inc., a Delaware corporation.

“NYSE” means the New York Stock Exchange.

“PIPE Financing” means the private placement pursuant to which the PIPE Investors collectively subscribed for 15,500,000 shares of our common stock at $10.00 per share, for an aggregate purchase price of $155,000,000, on the Closing.

“PIPE Investors” means certain institutional investors that invested in the PIPE Financing.

“PIPE Shares” means the 15,500,000 shares of our common stock issued in the PIPE Financing.

“private placement warrants” means the 4,450,000 warrants originally issued to the Sponsor in a private placement in connection with our IPO.

“public shares” means the Class A ordinary shares included in the units issued in our IPO.

“public shareholders” means holders of public shares.

“public warrants” means the 8,625,000 warrants included in the units issued in our IPO.

“Sarbanes-Oxley Act” or “SOX” means the Sarbanes-Oxley Act of 2002.

“SEC” means the United States Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Sponsor” means Spitfire Sponsor LLC, a Delaware limited liability company.

“Subscription Agreements” means, collectively, those certain subscription agreements, entered into on March 22, 2021, between the Company and the PIPE Investors.

“Trust Account” means the trust account of the Company that held the proceeds from the IPO and a portion of the proceeds from the sale of the private placement warrants.

“Velo3D” refers to Velo3D, Inc., a Delaware corporation (f/k/a JAWS Spitfire Acquisition Corporation, a Cayman Islands exempted company), and its consolidated subsidiary following the Closing.

In addition, unless otherwise indicated or the context otherwise requires, references in this Annual Report to the “Company,” “we,” “us,” “our,” and similar terms refer to Legacy Velo3D prior to the Merger and to Velo3D and its consolidated subsidiary after giving effect to the Merger.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this Annual Report may constitute “forward-looking statements” for purposes of the federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “can,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “will,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this Annual Report may include, for example, statements about:

•our projected financial information, growth rate and market opportunity;

•the ability to maintain the listing of our common stock and the public warrants on the NYSE, and the potential liquidity and trading of such securities;

•the ability to recognize the anticipated benefits of the Merger, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitably and retain its key employees;

•costs related to the Merger;

•changes in applicable laws or regulations;

•the inability to develop and maintain effective internal control over financial reporting;

•our ability to raise financing in the future;

•our success in retaining or recruiting, or changes required in, our officers, key employees or directors;

•the period over which we anticipate our existing cash and cash equivalents will be sufficient to fund our operating expenses and capital expenditure requirements;

•the potential for our business development efforts to maximize the potential value of our portfolio;

•regulatory developments in the United States and foreign countries;

•the impact of laws and regulations;

•our estimates regarding expenses, future revenue, capital requirements and needs for additional financing;

•our financial performance;

•the effect of COVID-19, and variant strains of the virus, on the foregoing; and

•other factors detailed under the section entitled “Risk Factors”.

The forward-looking statements contained in this Annual Report are based on current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the section entitled “Risk Factors”. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Some of these risks and uncertainties may in the future be amplified by the COVID-19 outbreak and there may be additional risks that we consider immaterial or which are unknown. It is not possible to predict or identify all such risks. We do not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

PART I

Item 1. Business.

Overview

We seek to fulfill the promise of additive manufacturing, also referred to as 3D printing ("AM"), to deliver breakthroughs in performance, cost and lead time in the production of high-value metal parts.

We produce a full-stack hardware and software solution based on our proprietary laser powder bed fusion ("L-PBF") technology, which enables support-free production. Our technology enables the production of highly complex, mission-critical parts that existing AM solutions cannot produce without the need for redesign or additional assembly. Our products give our customers who are in space, aviation, defense, energy and industrial markets the freedom to design and produce metal parts with complex internal features and geometries that had previously been considered impossible for AM. We believe our technology is years ahead of competitors.

Our technology is novel compared to other AM technologies based on its ability to deliver high-value metal parts that have complex internal channels, structures and geometries. This affords a wide breadth of design freedom for creating new metal parts and it enables replication of existing parts without the need to redesign the part to be manufacturable with AM. Because of these features, we believe our technology and product capabilities are highly valued by our customers. Our customers are primarily original equipment manufacturers ("OEMs") and contract manufacturers who look to AM to solve issues with traditional metal parts manufacturing technologies. Those traditional manufacturing technologies rely on processes, including casting, stamping and forging, that typically require high volumes to drive competitive costs and have long lead times for production. Our customers look to AM solutions to produce assemblies that are lighter, stronger and more reliable than those manufactured with traditional technologies. Our customers also expect AM solutions to drive lower costs for low-volume parts and substantially shorter lead times. However, many of our customers have found that legacy AM technologies failed to produce the required designs for the high-value metal parts and assemblies that our customers wanted to produce with AM. As a result, other AM solutions often require that parts be redesigned so that they can be produced and frequently incur performance losses for high-value applications. For these reasons, AM solutions of our competitors have been largely relegated to tooling and prototyping or the production of less complex, lower-value metal parts.

In contrast, our technology can deliver complex high value metal parts with the design advantages, lower costs and faster lead times associated with AM, and generally avoids the need to redesign the parts. As a result, our customers have increasingly adopted our technology into their design and production processes. We believe our value is reflected in our sales patterns, as most customers purchase a single machine to validate our technology and purchase additional systems over time as they embed our technology in their product roadmap and manufacturing infrastructure. We consider this approach a “land and expand” strategy, oriented around a demonstration of our value proposition followed by increasing penetration with key customers.

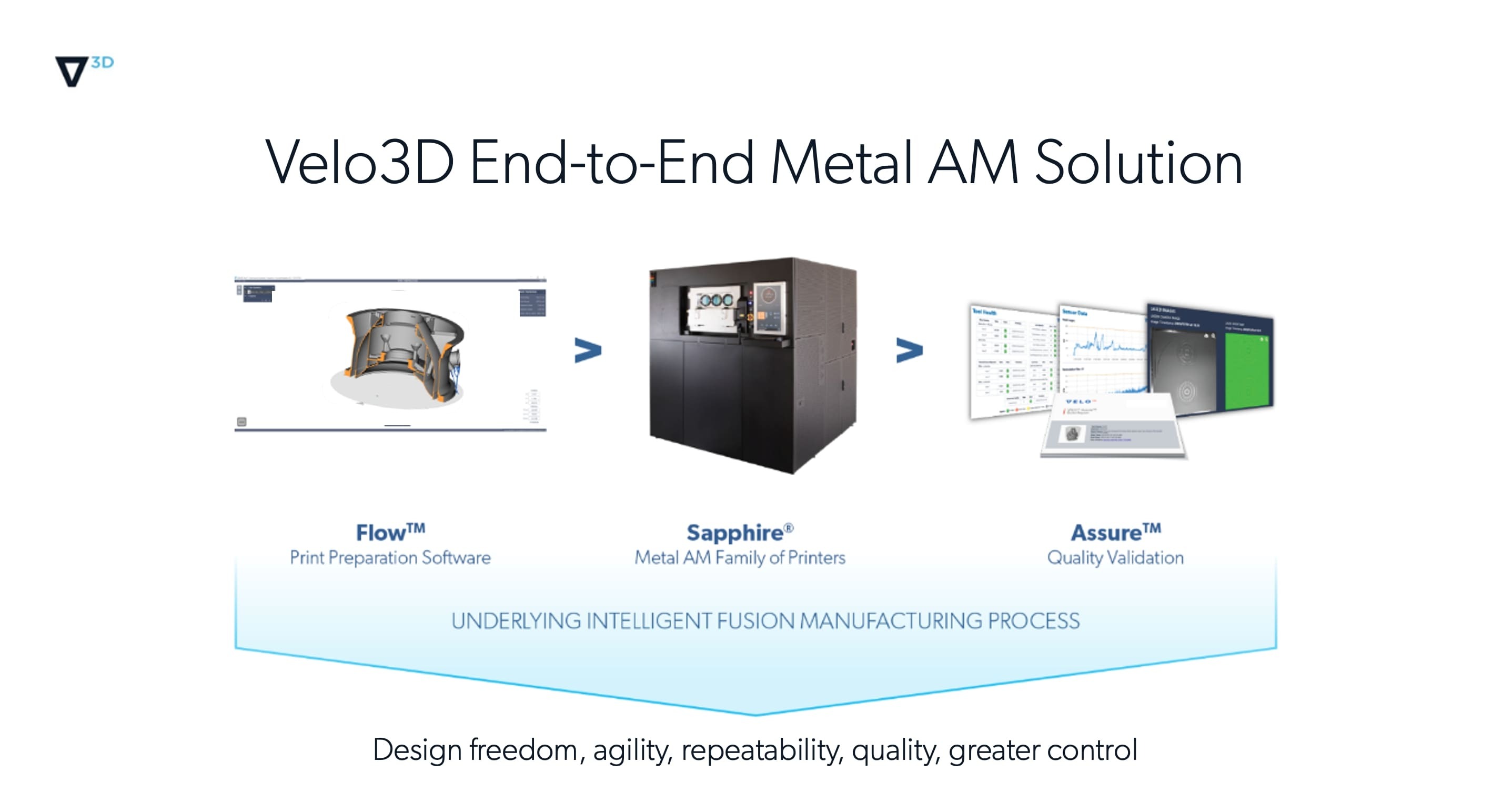

We offer customers a full-stack solution, which includes the following key components:

•Flow™ print preparation software conducts sophisticated analysis of the features of the metal part and specifies a production process that enables support-free printing of the part.

•Sapphire® metal AM printers produce the part using our proprietary L-PBF technology, which enables support-free designs. Our technology produces metal parts by fusing many thousands of very thin layers of metal powder with a precisely controlled laser beam in a sophisticated software defined sequence (or “recipe”) defined by our Flow™ software.

•Assure™ quality validation software validates the product made by Sapphire® to confirm that it is made to the specifications required by the original design.

Legacy AM technologies often rely on internal supports to prevent deformation of the metal part during the 3D printing process. These supports inhibit the production of parts with complex internal geometries, which are often required in high-performance applications, because there is limited or no access to remove them after production. Our technological advances enable our Sapphire® product to print metal parts that do not require internal supports, which enables our customers to produce designs that would otherwise be infeasible to make with AM.

We sell our full-stack hardware and software AM solutions through two types of transaction models: a 3D printer sale transaction and a recurring payment transaction. 3D printer sale transactions are structured as a payment of a fixed purchase price for the system. Recurring payment transactions fall into two categories: a leased 3D printer

transaction and a sale and utilization fee model. Under the leased 3D printer transaction, the customer typically pays an amount for a lease which entitles the customer to a base number of hours of usage. For usage above that level, the customer typically pays an hourly usage fee. Most of our leases have a 12-month term, though in certain cases the

lease term is longer. In the sale and utilization fee model, customers pay an upfront amount that is less than the full purchase price to purchase the system. This purchase price is supplemented by an hourly usage fee for each hour of system utilization over the life of the system. The variable payments are recognized when the event determining the amount of variable consideration to be paid occurs. Support services are included with a 3D printer sale transaction and a recurring payment transaction.

We delivered our first Sapphire® XC system at the end of 2021. We continue to see strong demand for our next-generation flagship Sapphire® XC product. It is anticipated that this product compared to our existing Sapphire® system will be able to increase throughput by up to 400%, reduce part costs by 65% to 80% and expand part size capacity by up to 4 times. Together, the increase in capabilities and improvement in economics for our customers is anticipated to rapidly increase the potential applications of our technology. As of December 31, 2021, our aggregate backlog for the Sapphire® XC was $43 million, comprised of 18 Sapphire® XC systems. Demand for the Sapphire® XC product is a significant contributor to our expectation for meaningful sales growth from 2022 and beyond.

Strategy for Growth

The key elements for our growth strategy include the following:

Focus on uncontested segments of the market

We focus our sales efforts on customers with a need for parts which our proprietary L-PBF technology can produce but which cannot be produced by competitors’ AM technology. These include high-performance metal parts with complex internal geometries, including critical components within jet engines, fuel delivery systems and heat exchangers. These parts are fundamentally out of reach for other AM suppliers serving the high-value metal parts segment because their production process requires internal supports for complex internal geometries, which cannot be removed. Likewise, the processes required by traditional metal manufacturing processes (for example, welding of multiple parts into the desired assembly) often result in parts with lower performance, higher cost and/or longer lead times than the parts which our solution can produce. We generally do not compete in the segment of the AM market composed of applications which can be served by the multiple existing competitors in metal AM. Our primary focus is on those applications where demand for our solution is expected to be the strongest, thus supporting our long-term margins.

Increase penetration with customers as part of a “land and expand” strategy

We adopt a two-step approach to customer relationships, whereby we first aim to validate our technology with customers before working to more fully integrate our technology into customers’ designs and/or production processes. Upon building a strong customer relationship, our sales personnel and engineers collaborate with their customer counterparts to identify how our technology can add the greatest value to the customer’s ultimate product. We have found that this helps customers to best understand the potential for the wide breadth of design freedom that our products can deliver, which often leads to customers fully integrating our technology into their processes and making multiple follow-on purchases. This results in economies of scale, as fewer sales and engineering personnel are able to serve a larger number of machines that are concentrated with a smaller number of customers. In addition, by integrating our technology into customer designs, we effectively expand the uncontested market which we believe we are optimally suited to serve.For the last two years we have delivered, on average, 1.3 Sapphire® systems per existing customer at the beginning of the year.

Accelerate global acquisition of new customers

We plan to increase the number of customer relationships we have globally in the coming years both organically and through distribution partnerships. In recent years, we have demonstrated that our technology can bring tremendous value across a number of use cases in the space, aviation and defense, energy and industrial segments. We plan to leverage the success from these deployments into sales to a number of new customers by ramping our sales force in the coming years to allow for the continued execution of our “land and expand” strategy.

Since 2019, we have also established relationships with distribution partners in the Asia-Pacific region (Taiyo Nippon Sanso Corporation and Avaco) and in the U.S. (GoEngineer) and sales agents in the Middle East and Africa to provide greater leverage to our sales team and enable expansion into new markets. We will continuously evaluate other potential distribution partnerships to further increase our footprint. Going forward, we may consider acquisitions of other AM solution providers to acquire new customer relationships.

Adopt multiple revenue models to fit customer preferences

We plan to adopt sales models that align with our customers’ financial preferences to increase total units sold and optimize our margin profile. Our target customers include several OEMs with vertically integrated operations, as well as a larger number of contract manufacturers who are part of diverse supply chains. Our 3D printer sale transactions include a higher up-front price for our system and a lower annual service fee, and are typically preferred by the vertically integrated OEMs, who often seek to minimize total cash outlays. We also have recurring payment transactions, including a sale and utilization fee model, where customers pay an up-front amount that is less than the full purchase price to purchase the system. This purchase price is supplemented by an hourly usage fee for each hour of system utilization over the life of the system. We believe the recurring payment model may be preferred by contract manufacturers, because the payment structure is better matched to their revenue stream. We believe these customers offer significant opportunities in particular, as SmarTech expects that demand for high-value metal parts from contract manufacturers will grow by 32% from 2021 to 2026.

Rapidly scale to meet customer demand

We plan to scale our business quickly to meet the significant increase in demand that we have seen from our customers by increasing the number of sales representatives and engineers to serve those customers, as well as our production capacity. Our manufacturing operations are limited to the final assembly and test of the system. Components and sub-assemblies are sourced from suppliers. As a result, we have the ability to scale our manufacturing operations with relatively limited capital investment because we only require additional assembly and warehouse space to increase our manufacturing capacity. Further, because our business model is capital efficient, we are able to adapt to shifts in customer demand and calibrate our growth plans to ensure that we maintain the appropriate production capacity at all times.

Extend competitive advantage with new products and continued R&D

We plan to accelerate our research and development ("R&D") efforts in the future to further extend our technological advantage relative to our competitors. We have spent approximately $175 million over the past seven years in R&D. The latest iteration of our product is our Sapphire® XC system, which launched at the end of 2021. This product will represent a step-function improvement in part size capability and productivity relative to our existing product offerings. Compared to Sapphire®, Sapphire® XC is able to produce parts that are 400% larger in volume and reduce the cost of parts produced on the system by approximately 65% to 80%. We believe this will increase considerably the range of applications where our manufacturing technology will be competitive with traditional metal manufacturing techniques, thereby substantially expanding our addressable market.

Our Competitive Strengths

Disruptive AM platform with the unique ability to produce complex designs without internal supports

In contrast to other L-PBF technologies, our proprietary L-PBF technology is capable of producing metal parts with complex internal geometries. Manufacturers of high-performance products have looked to AM to improve performance, reduce costs and shorten lead times relative to traditional metal parts manufacturers; however, other AM solutions have been historically limited because they must use internal supports to enable production of the part. Our technology delivers on the promise of AM, allowing customers a wide breadth of freedom to design products with optimal performance characteristics. In addition to greater design freedom, our technology allows customers to consolidate assemblies of multiple metal parts into a single part that delivers a stronger, lighter, better performing part at a lower cost than possible through traditional metal manufacturing techniques. Finally, our solutions enable

the production of high-value, low-volume spare parts on demand, which may result in meaningful reductions to requirements for inventory. These factors create an uncontested segment in the market with customers we are ideally positioned to serve.

Existing relationships with blue chip customers across our target end markets

We have built relationships with blue chip customers across all of our target industries, including space , aviation and defense, energy and other industrial applications. Except for SpaceX, these are our indirect customers who specify our 3D printers for the manufacture of components by contract manufacturers that use our 3D printers and, while these customers provide no direct revenue to the Company, they drive part of the volume for our contract manufacturers and therefore, indirectly, our 3D printer demand. We have built these relationships by demonstrating the value that our differentiated technology can achieve and integrating our solutions into their operations, resulting in repeat sales to multiple customers within a short span of time. Our success in partnering with existing customers has also validated our differentiated technology for other potential customers. We believe that our successes with these efforts provide meaningful proof of concept and will enable our strategy of rapid customer acquisition in the coming years.

End-to-End, turnkey solution that can be easily integrated into customer operations

Our end-to-end solution can be integrated into customer operations with relative ease, facilitating adoption with new customers, as well as the installation of additional systems. The turnkey nature of our products effectively enables our “land and expand” strategy. We typically dedicate one engineer for several weeks around the time of the installation to educate customers as to how to best use our systems and to identify how our technology can most effectively add value to customer processes. After this point, our customers become largely self-supported, requiring only occasional support from our sales and engineering staff. This enables us to effectively reallocate our engineers and salesforce to continue to engage with new potential customers, supporting our efforts to scale our operations rapidly.

Deep moat of intellectual property protections

We have a strong, multi-layered portfolio protecting our intellectual property (“IP”) rights, which reinforces our competitive advantage. According to SmarTech, as of 2019, we have the strongest IP portfolio in metal additive manufacturing (AM): “Velo3D and . . . have impressive patent portfolios. Some of the most impressive patent portfolios are held by smaller firms. Velo3D is currently the top assignee of patents for 3D printing metals,” SmarTech Analysis Announces New Report on 3D-Printed Metals Patents, Smartchechanalysis.com, July 22, 2019. As of December 31, 2021, our multi-jurisdictional patent IP portfolio includes 54 patents that have been granted across systems, methods, devices, apparatuses, software, and compositions of matter (e.g., 3D objects), as well as 11 public pending patent applications. This IP portfolio enables us to prevent third-party market participants from selling our patented systems, using our patented production methods, or trading in parts that have been made using our processes. Our multi-jurisdictional trademark IP portfolio includes 23 registered trademarks and 39 pending trademark applications. This IP portfolio enables us to defend our unique brand from our competitors in the various jurisdictions. Accordingly, we expect that our strong IP portfolio will enable us to protect our technological lead in the metal AM industry and the unique brand we market to our customers and potential customers.

Capital efficient business model

We have an asset-light business model, which will allow us to scale our operations to meet expected customer demand. Our own manufacturing operations are primarily limited to final assembly, testing and shipment. Further, we believe our units are higher value and lower volume relative to other AM solutions providers, which reduces the burden on our supply chain as we expand. Our final assembly process does not require expensive clean rooms but instead occurs within an assembly facility. We believe that this will enable us to rapidly scale our business model to meet customer demand, without the risks associated with other manufacturing models that require heavy capital expenditures to increase production capacity.

Experienced management team

Our management team has decades of relevant experience across their respective industries, including materials engineering, technological development, operations, sales, business development and corporate finance. Our management team is led by our Chief Executive Officer, Benny Buller, who has had a highly successful career as an engineer, culminating in the highest Israeli Presidential award for one of the projects he led in the Israeli intelligence community, before taking leadership positions in cutting-edge American technology firms, including in First Solar and Applied Materials. Our Chief Financial Officer, Bill McCombe, has extensive experience as a senior financial officer in public and private technology hardware companies and as a senior investment banker overseeing strategic transactions. Further, we have recently added experienced independent board members to support our management team.

Our Product Platforms

Since our founding in 2014, we have focused development on our primary solution, marketed as Sapphire®. Sapphire® is an end-to-end solution and comes with the Flow™ design software and Assure™ quality control software. At the end of 2021, we launched our new Sapphire® XC product, which will enable production of larger parts at a lower cost.

Our software is fully integrated into the design, production and quality control platform with our Sapphire® and Sapphire® XC systems. We maintain legal title of our software systems for products sold under both our 3D printer sale transactions and recurring payment transactions.

Flow™

Flow™ software powers the whole family of Sapphire® AM printers. Our systems rely on the same manufacturing process for all of our printer solutions. Flow™ is a highly advanced and proprietary software platform, which scans part designs for unique geometrical features. It uses advanced computational algorithms to prescribe specific manufacturing “recipes” and processes specific to the Sapphire® production systems to ensure that the part is produced with the required specifications.

Sapphire® and Sapphire® XC

The Sapphire® printer system is our first generation production machine. As of December 31, 2021, 46 machines have been shipped and are currently in the field. Sapphire® uses L-PBF technology and supports a build module of 315 millimeter diameter by 400 millimeter tall, and volume of up to 31 liters.

Sapphire® XC is our newest generation of printer and started shipping at the end of 2021. XC stands for “extra capacity” and has a larger build module of 600 millimeter diameter by 550 millimeter tall, and volume of up to 155 liters. Sapphire® XC is based on the same fundamental design of our original Sapphire® printers. The Sapphire® XC printer system is designed with the intent that all recipes and parts designed for the original Sapphire® printers are fully compatible with the Sapphire® XC printer systems, as the new system is designed to carry over processes and metrologies.

Our machines have the ability to make parts with thousands of composite structures, including titanium, nickel-alloys, nickel super alloys, steel and steel alloys. Any metal that is cold-weldable is able to be used as a base layer in our machines. We currently have recipes for nine alloys and add recipes for additional metal alloys based on customer demand.

Assure™

Assure™ is an advanced quality control system software platform that includes process metrologies to ensure repeatable, consistent part quality. The platform works with complex sensors, which allow prompt control modulation of the Sapphire® laser systems to calibrate production outcomes within tolerances.

Intelligent Fusion®

Intelligent Fusion® is the underlying manufacturing process that binds and facilitates all aspects of the Velo3D end-to-end solution, which includes our print preparation software (Flow™), advanced metal 3D printers (Sapphire®), and quality assurance software (Assure™).

Intelligent Fusion® unifies and manages all of the above, including the information flow, sensor data from over 950 sensors, and the advanced printing technology for precision control of the entire print.

Customers

Our customers range from small- and medium-sized enterprises to Fortune 500 companies in the space, aviation, defense, energy and industrial markets. As of December 31, 2021, we had 18 customers. We added 10 new customers in 2021, and we continue to diversify our customer base. SpaceX, our largest customer, accounted for 27.8% and 41.1% of our revenue for the year ended December 31, 2021 and 2020, respectively. Our customers include both OEMs, as well as contract manufacturers who provide service and parts on behalf of OEMs. Our 3D printer sales occur under purchase orders that are governed by our terms and conditions of sale. The Company’s terms and conditions with SpaceX are consistent with all other customers and permit the customers to terminate the Company’s services at any time (subject to notice and certain other provisions).

We only sell to production customers. Our machines are not resalable and software licenses are not transferable to certain geographic markets to protect our IP.

Research and Development

The high-value metal parts and AM segments are undergoing technological advancements across hardware, software and materials. We continue to dedicate meaningful resources into our ongoing R&D programs to extend our technological leadership. Specifically, our R&D team is focused on continuing advances in technology that include, but are not limited to:

•enhancements of the Sapphire® systems, such as 1MZ systems;

•improvement of reliability and productivity of the Sapphire® and Sapphire® XC systems;

•expansion of functionality of Flow™ software;

•qualifying new materials;

•additional quality control features in Assure™; and

•addition of recipes for new metal alloys.

We invest a significant amount of our resources in R&D because we believe that superior technology is a key to maintaining a leading market position. In the year ended December 31, 2021 and 2020, our R&D expenses were approximately $27.0 million and $14.2 million.

Sales and Marketing

We sell our AM solutions directly, as well as through a network of multiple distribution partners. Together, these relationships span much of the world, including the United States ("U.S."), the EU, Japan, South Korea and Southeast Asia. We engage in a “land and expand” strategy, whereby we seek to make an initial sale to customers for technology validation before increasing penetration through sales of additional units.

Our marketing strategy is oriented around building deep and lasting relationships with leading global manufacturers. We seek to compete by maximizing the value we create for our customers. To that end, our engineers engage with customers to identify the specific parts and processes where our solutions can add the most immediate value. At the time of the installation, our engineers will typically engage with customers for several weeks to educate them on the system, after which point customers are typically able to operate the system without our direct engagement.

Our sales team remains engaged with customers after initial validation of our technology with a goal of integrating our technology into other customer processes. Thus far, we believe this strategy has proven successful, for the last two years we have delivered, on average, 1.3 Sapphire® systems per existing customer at the beginning of the year . As of February 28, 2021, our sales and marketing teams consisted of 28 employees.

In recent years, we have successfully demonstrated the utility of our technology across multiple target markets, including the highest performance application in the space, aviation and defense, energy and industrial end markets. We believe these successful deployments have seeded the market and will enable increased acquisition of new customers in those segments.

We rely on our own sales team, as well as multiple distribution partners, including Taiyo Nippon Sanso (Japan), Avaco (South Korea), and GoEngineer (North America). These relationships have helped to extend our reach into overseas markets and essentially function as extensions of our sales team. We have entered into partnership agreements with each of our distribution partners, which grant the distribution partner the right to market our products in a specified territory on either an exclusive or nonexclusive basis, depending on the distribution partner; however, all sales contracts for our products are entered into between us and our customers. Certain of these distribution partners also provide maintenance services to customers in their specified territories. Going forward, we plan to expand our direct sales force and will consider establishing additional distribution partnerships as we continue to implement our strategy with new customers.

In the fourth quarter of 2021, we opened our European Headquarters at the Augsburg Innovation Park, located in Augsburg, Germany, that will include teams of sales, application engineering and field service engineering personnel, similar to the U.S. office.

Manufacturing and Suppliers

We design, assemble, test and ship all of our products and rely on outside manufacturers for component manufacturing. Production of our systems requires approximately 15 weeks. We employ several third-party vendors to supply our core hardware subsystems and components. Following receipt of these subsystems and components, we assemble and calibrate the system. We then conduct a series of process tests culminating in a final factory acceptance test. We have internal teams focused on technology development, engineering and manufacturing. The teams coordinate the design, construction, assembly, testing and shipment of our products.

We currently rely on numerous external suppliers, which we believe have ample capacity to increase supply of our critical components. For the majority of these suppliers, we believe we can readily source components from competing suppliers on short notice. As our business grows, we may consider a strategy of sourcing components from multiple suppliers to ensure surety of supply.

We manage our inventory based on sales and production forecasts and anticipated lead times for sourcing components and assembly.

Intellectual Property

Our leadership in the high-value metal parts AM segment depends largely on our differentiated technology, which we seek to protect through a multi-layered IP approach. Our IP protection enables us to prevent organizations and individuals from selling or using our systems, apparatuses, devices, and software, practicing our methods, or trading in our produced parts (e.g., 3D objects), as these are all protected by various forms of IP protection including by our patents granted in various jurisdictions and by our trade secrets.

We attempt to protect our IP rights, in various jurisdictions (e.g., United States and abroad), through a combination of patents, trademarks, copyrights and trade secrets, as well as nondisclosure and invention assignment agreements with our consultants and employees, and nondisclosure agreements with our contractors, vendors and other business partners.

We pursue patent protection when we believe it is possible and consistent with our overall strategy for safeguarding IP.

Our patent profile is a broad portfolio across our systems, apparatuses, devices, methods (e.g., of production), software, and composition of matter (e.g., 3D objects). Metal parts produced using our system technology have a signature that is readily recognizable and traceable. According to SmarTech, as of 2019, we have the strongest IP portfolio in metal AM: “Velo3D and . . . have impressive patent portfolios. Some of the most impressive patent portfolios are held by smaller firms. Velo3D is currently the top assignee of patents for 3D printing metals,” SmarTech Analysis Announces New Report on 3D-Printed Metals Patents, Smartchechanalysis.com, July 22, 2019.

We own fifty-four (54) issued patents of which forty (40) are issued U.S. patents, and fourteen (14) are issued foreign patents. We also have eleven (11) public pending patent applications of which one (1) is a pending U.S. patent application, eight (8) are pending public foreign patent applications, and two (2) are public pending Patent Cooperation Treaty (PCT) patent applications. Our currently issued patents will expire at different times in the future, with the earliest expiring in 2035 and the latest expiring in 2039. Our currently pending applications will generally remain in effect for 20 years from the date of filing of the initial patent application of each. In addition, we have four (4) registered U.S. trademarks, nineteen (19) registered foreign trademarks, one (1) pending U.S. trademark applications, and thirty-eight (38) pending foreign trademark applications.

Human Capital Resources

We have a strong team of employees who contribute to our success. As of December 31, 2021, we had 193 full-time employees, the majority of them based at our headquarters. We rely on consultants and outside contractors in roles and responsibilities that include engineering, operations and finance.

To date, we have not experienced any work stoppages and consider our relationship with our employees to be in good standing, as evidenced by our recent employee engagement score in February 2022, which was 4 percentage points higher than the industry benchmark per a December 2021 employee survey conducted by Energage. None of our employees are subject to a collective bargaining agreement or are represented by a labor union.

Our board of directors oversees matters relating to managing our human capital resources. Our human capital resources objectives include identifying, recruiting, retaining, training, incentivizing and integrating our existing and additional employees, as well as emphasizing work place safety. We review our compensation and benefit policies regularly through industry benchmarks and, we believe we offer competitive compensation and benefits packages, the principal purposes of which are to attract, retain and motivate our employees.

Competition

We compete with other suppliers of 3D printers, materials and software, as well as with suppliers of traditional metal manufacturing solutions. We compete with these suppliers, as well as channel partners, for customers, and for certain of our products. We also compete with businesses and service bureaus that use such equipment to produce models, prototypes, molds and end-user parts. Development of new technologies or techniques not encompassed by the patents that we own may result in additional future competition.

Our competitors operate both globally and regionally, and many of them have well-recognized brands and product lines. Additionally, certain of our competitors are well established and may have greater financial resources than us.

We believe principal competitive factors include technology capabilities, materials, process and application know-how, total cost of operation of solution, product reliability and the ability to provide a full range of products and services to meet customer needs. We believe that our future success depends on our ability to provide high-quality solutions, introduce new products and services to meet evolving customer needs, market opportunities, and extend our technologies to new applications. Accordingly, our ongoing R&D programs are intended to enable us to continue technology advancement and develop innovative new solutions for the marketplace.

Government Regulations

We are subject to various laws, regulations and permitting requirements of U.S. federal, state and local and foreign authorities. These include:

•regulations promulgated by environmental and health agencies, as described below under “- Environmental Matters”;

•the U.S. Occupational Safety and Health Administration;

•the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act and the anti-corruption laws of other countries;

•laws pertaining to the hiring, treatment, safety and discharge of employees; and

•import and trade restrictions and export control regulations, including the U.S. International Traffic in Arms Regulations and the U.S. Export Administration Regulations.

We believe that we are in material compliance with all such laws, regulations and permitting requirements.

Environmental Matters

We are subject to various environmental, health and safety laws, regulations and permitting requirements, including those governing the emission and discharge of hazardous materials into ground, air or water; noise emissions; the generation, storage, use, management and disposal of hazardous and other waste; the import, export and registration of chemicals; the cleanup of contaminated sites; and the health and safety of our employees. Based on information currently available to us, we do not expect environmental costs and contingencies to have a material adverse effect on our operations. The operation of our facility, however, entails risks in these areas. Significant expenditures could be required in the future to comply with environmental or health and safety laws, regulations or other requirements. Certain of these compliance requirements are imposed by our customers, who at times require us to be registered with U.S. health or safety regulatory agencies, whether on the federal or state level.

Under environmental laws and regulations, we are required to obtain environmental permits from governmental authorities for certain operations.

In the European marketplace, among others, electrical and electronic equipment is required to comply with the Directive on Waste Electrical and Electronic Equipment of the EU, which aims to prevent waste by encouraging reuse and recycling, and the EU Directive on Restriction of Use of Certain Hazardous Substances, which restricts the use of various hazardous substances in electrical and electronic products. Our products and certain components of such products “put on the market” in the EU (whether or not manufactured in the EU) are subject to these directives. Additionally, we are required to comply with certain laws, regulations and directives governing chemicals, including the U.S. Toxic Substances Control Act, Registration, Evaluation, Authorisation and Restriction of Chemicals (“REACH”), the Restriction of Hazardous Substances Directive (“RoHS”) and Classification, Labelling and Packaging Regulation (“CLP”) in the EU. These and similar laws and regulations require, among others, the registration, evaluation, authorization and labeling of certain chemicals that we use and ship.

Corporate Information

We were incorporated on September 11, 2020 as a special purpose acquisition company and a Cayman Islands exempted company under the name JAWS Spitfire Acquisition Corporation. On December 7, 2020, JAWS Spitfire completed its initial public offering. On September 29, 2021, JAWS Spitfire consummated the Merger with Legacy Velo3D pursuant to the Business Combination Agreement. In connection with the Merger, JAWS Spitfire’s jurisdiction of incorporation was changed from the Cayman Islands to the State of Delaware, and JAWS Spitfire changed its name to Velo3D, Inc.