Filed Pursuant to Rule 424(b)(3)

Registration No. 333-260415

PROSPECTUS

Velo3D, Inc.

169,147,569 Shares of Common Stock

4,450,000 Warrants to Purchase Shares of Common Stock

13,075,000 Shares of Common Stock Underlying Warrants

This prospectus relates to the offer and sale from time to time by the selling securityholders named in this prospectus (the “Selling Securityholders”) of (A) up to 169,147,569 shares of our common stock, par value $0.00001 per share (our “common stock”), consisting of (i) up to 15,500,000 shares of our common stock (the “PIPE shares”) issued in a private placement pursuant to subscription agreements each entered into on March 22, 2021 (the “PIPE Financing”); (ii) up to 8,625,000 shares of our common stock (the “Founder Shares”) issued in connection with the consummation of the Business Combination (as defined below), in exchange for our Class B ordinary shares originally issued in a private placement to Spitfire Sponsor LLC (the “Sponsor”); (iii) up to 140,572,569 shares of our common stock issued or issuable to certain former stockholders and equity award holders of Velo3D (the “Velo3D equity holders”) in connection with or as a result of the consummation of the Business Combination, consisting of (a) up to 123,058,137 shares of our common stock; (b) up to 1,902,945 shares of our common stock issuable upon the exercise of certain options; and (c) up to 15,611,487 shares of our common stock (the “Earn-Out Shares”) that certain Velo3D equity holders have the contingent right to receive upon the achievement of certain vesting conditions; and (iv) up to 4,450,000 shares of our common stock issuable upon the exercise of the private placement warrants (as defined below); and (B) up to 4,450,000 warrants (the “private placement warrants”) originally issued in a private placement to the Sponsor.

In addition, this prospectus relates to the offer and sale of: (i) up to 8,625,000 shares of our common stock that are issuable by us upon the exercise of 8,625,000 warrants (the “public warrants”) originally issued in our initial public offering (the “IPO”); and (ii) up to 4,450,000 shares of our common stock that are issuable by us upon the exercise of the private placement warrants.

On September 29, 2021 (the “Closing Date”), we consummated the transactions contemplated by that certain Business Combination Agreement, dated as of March 22, 2021 (as amended, the “Business Combination Agreement”), by and among JAWS Spitfire Acquisition Corporation (“JAWS Spitfire” and, after the consummation of the Business Combination, “New Velo3D”), Spitfire Merger Sub, Inc. (“Merger Sub”) and Velo3D, Inc. (“Velo3D”). In particular, as contemplated by the Business Combination Agreement, on the Closing Date, JAWS Spitfire filed a notice of deregistration with the Cayman Islands Registrar of Companies, together with the necessary accompanying documents, and filed a certificate of incorporation and a certificate of corporate domestication with the Secretary of State of the State of Delaware, under which JAWS Spitfire was domesticated and continued as a Delaware corporation (the “Domestication”). Further, as contemplated by the Business Combination Agreement, on the Closing Date, Merger Sub was merged with and into Velo3D, with Velo3D surviving the merger (the “Surviving Corporation”) as a wholly-owned subsidiary of us (the “Merger” and, together with the Domestication and the other transactions contemplated by the Business Combination Agreement, including the PIPE Financing, the “Business Combination”). In connection with the consummation of the Business Combination, we changed our name to “Velo3D, Inc.” and the Surviving Corporation changed its name to “Velo3D US, Inc.”

The Selling Securityholders may offer, sell or distribute all or a portion of the securities hereby registered publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from such sales of the shares of our common stock or warrants, except with respect to amounts received by us upon the exercise of the warrants for cash. We will bear all costs, expenses and fees in connection with the registration of these securities, including with regard to compliance with state securities or “blue sky” laws. The Selling Securityholders will bear all commissions and discounts, if any, attributable to their sale of shares of our common stock or warrants. See “Plan of Distribution” beginning on page 130 of this prospectus.

Our common stock and public warrants are listed on the New York Stock Exchange (the “NYSE”) under the symbols “VLD” and “VLD WS”, respectively. On October 26, 2021, last reported sales price of our common stock was $9.85 per share and the last reported sales price of our public warrants was $1.91 per warrant.

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, and, as such, have elected to comply with certain reduced disclosure and regulatory requirements.

Investing in our securities involves risks. See the section entitled “Risk Factors” beginning on page 11 of this prospectus to read about factors you should consider before buying our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is October 28, 2021

TABLE OF CONTENTS

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, the Selling Securityholders may, from time to time, sell or otherwise distribute the securities offered by them as described in the section titled “Plan of Distribution” in this prospectus. We will not receive any proceeds from the sale by such Selling Securityholders of the securities offered by them described in this prospectus. This prospectus also relates to the issuance by us of the shares of common stock issuable upon the exercise of any warrants. We will receive proceeds from any exercise of the warrants for cash.

Neither we nor the Selling Securityholders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Securityholders take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Securityholders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the sections of this prospectus entitled “Where You Can Find More Information.”

Unless the context otherwise requires, references in this prospectus to references to:

•“JAWS Spitfire” refer to JAWS Spitfire Acquisition Corporation, a Cayman Islands exempted company, prior to the Closing (as defined herein);

•“New Velo3D” refer to Velo3D, Inc., a Delaware corporation (f/k/a JAWS Spitfire Acquisition Corporation, a Cayman Islands exempted company), and its consolidated subsidiary following the Closing;

•“Velo3D” refer to Velo3D, Inc., a Delaware corporation, prior to the Closing; and

•“we,” “us,” and “our” or the “Company” refer to New Velo3D following the Closing and to Velo3D prior to the Closing.

SELECTED DEFINITIONS

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

“Board” or “Board of Directors” means the board of directors of the Company.

“Bylaws” means the restated bylaws of the Company.

“Business Combination” means the transactions contemplated by the Business Combination Agreement, including the Domestication, the Merger and the PIPE Investment.

“Business Combination Agreement” means that certain Business Combination Agreement, dated as of March 22, 2021, by and among JAWS Acquisition, Merger Sub and Velo3D, as amended by Amendment #1 to Business Combination Agreement dated as of July 20, 2021.

“Certificate of Incorporation” means the restated certificate of incorporation of the Company.

“common stock” means the shares of common stock, par value $0.00001 per share, of the Company.

“Class A ordinary shares” means the Class A ordinary shares, par value $0.0001 per share, of JAWS Spitfire, prior to the Domestication, which automatically converted, on a one-for-one basis, into shares of common stock in connection with the Closing.

“Class B ordinary shares” means the Class B ordinary shares, par value $0.0001 per share, of JAWS Spitfire, prior to the Domestication, which automatically converted, on a one-for-one basis, into shares of common stock in connection with the Closing.

“Closing” means the closing of the Business Combination.

“Closing Date” means September 29, 2021.

“Code” means the Internal Revenue Code of 1986, as amended.

“Company” means New Velo3D following the Closing and to Velo3D prior to the Closing.

“Domestication” means the domestication contemplated by the Business Combination Agreement, whereby JAWS Spitfire effected a deregistration and a transfer by way of continuation from the Cayman Islands to the State of Delaware, pursuant to which JAWS Spitfire’s jurisdiction of incorporation was changed from the Cayman Islands to the State of Delaware.

“DGCL” means the General Corporation Law of the State of Delaware.

“Earn-Out Shares” means up to 21,758,149 shares of our common stock issuable pursuant to the Business Combination Agreement to certain Velo3D equity holders upon the achievement of certain vesting conditions.

“Effective Time” means the time at which the Merger became effective.

“Equity Incentive Plan” means the Velo3D, Inc. 2021 Equity Incentive Plan.

“ESPP” means the Velo3D, Inc. 2021 Employee Stock Purchase Plan.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Founder Shares” means the 8,625,000 shares of our common stock issued to the Sponsor and the other Initial Stockholders in connection with the automatic conversion of the Class B ordinary shares in connection with the Closing.

“GAAP” means United States generally accepted accounting principles.

“Initial Stockholders” means the Sponsor together with Andy Appelbaum, Mark Vallely and Serena J. Williams.

“Investment Company Act” means the Investment Company Act of 1940, as amended.

“IPO” means the Company’s initial public offering, consummated on December 7, 2020, of 34,500,000 units (including 4,500,000 units that were issued to the underwriters in connection with the exercise in full of their over-allotment option) at $10.00 per unit.

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012.

“Merger” means the merger contemplated by the Business Combination Agreement, whereby Merger Sub merged with and into Velo3D, with Velo3D surviving the merger as a wholly-owned subsidiary of the Company on the Closing Date.

“Merger Sub” means Spitfire Merger Sub, Inc., a Delaware corporation.

“New Velo3D” refer to Velo3D, Inc., a Delaware corporation (f/k/a JAWS Spitfire Acquisition Corporation, a Cayman Islands exempted company), and its consolidated subsidiary following the Closing.

“NYSE” means the New York Stock Exchange.

“PIPE Financing” means the private placement pursuant to which the PIPE Investors collectively subscribed for 15,500,000 shares of our common stock at $10.00 per share, for an aggregate purchase price of $155,000,000, on the Closing.

“PIPE Investors” means certain institutional investors that invested in the PIPE Financing.

“PIPE Shares” means the 15,500,000 shares of our common stock issued in the PIPE Financing.

“private placement warrants” means the 4,450,000 warrants originally issued to the Sponsor in a private placement in connection with our IPO.

“public shares” means the Class A ordinary shares included in the units issued in our IPO.

“public shareholders” means holders of public shares.

“public warrants” means the 8,625,000 warrants included in the units issued in our IPO.

“Sarbanes-Oxley Act” or “SOX” means the Sarbanes-Oxley Act of 2002.

“SEC” means the United States Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Selling Securityholders” means the selling securityholders named in this prospectus.

“Sponsor” means Spitfire Sponsor LLC, a Delaware limited liability company.

“Subscription Agreements” means, collectively, those certain subscription agreements, entered into on March 22, 2021, between the Company and the PIPE Investors.

“Transfer Agent” means Continental Stock Transfer & Trust Company.

“Trust Account” means the trust account of the Company that held the proceeds from the IPO and a portion of the proceeds from the sale of the private placement warrants.

“Velo3D” means Velo3D, Inc., a Delaware corporation, prior to the Closing.

“Velo3D equity holder” means certain former stockholders and equity award holders of Velo3D.

MARKET AND INDUSTRY DATA

Information contained in this prospectus concerning the market and the industry in which we compete, including our market position, general expectations of market opportunity and market size, is based on information from various third-party sources, assumptions made by us based on such sources and our knowledge of the markets for our services and solutions. Any estimates provided herein involve numerous assumptions and limitations, and you are cautioned not to give undue weight to such information. Third-party sources generally state that the information contained in such source has been obtained from sources believed to be reliable but that there can be no assurance as to the accuracy or completeness of such information. These third party sources include the following reports and publications (the “Market and Industry Reports”):

•Investment Casting Market Size, Share & Trends Analysis Report By Application (Aerospace & Defense, Energy Technology), By Region (North America, Europe, APAC, Central & South America, MEA), And Segment Forecasts, 2020 – 2027, October 2020

•Market Research Future, Global Metal Forging Market, February 2021

•Technavio, Metal Machining Market by End-user and Geography 2020 – 2024, 2020

•ResearchAndMarkets.com, Braze Alloys – Global Market Trajectory & Analytics, April 2021

•SmarTech Analysis, Q3 2020 Market Report

The industry in which we operate is subject to a high degree of uncertainty and risk. As a result, the estimates and market and industry information provided in this prospectus are subject to change based on various factors, including those described in the section entitled “Risk Factors — Risks Related to Our Business” and elsewhere in this prospectus.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus may constitute “forward-looking statements” for purposes of the federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the Business Combination. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “can,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “will,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus may include, for example, statements about:

•our projected financial information, growth rate and market opportunity;

•the ability to maintain the listing of our common stock and the public warrants on the NYSE, and the potential liquidity and trading of such securities;

•the ability to recognize the anticipated benefits of the proposed Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitably and retain its key employees;

•costs related to the proposed Business Combination;

•changes in applicable laws or regulations;

•the inability to develop and maintain effective internal controls;

•our ability to raise financing in the future

•our success in retaining or recruiting, or changes required in, our officers, key employees or directors

•the period over which we anticipate our existing cash and cash equivalents will be sufficient to fund our operating expenses and capital expenditure requirements;

•the potential for our business development efforts to maximize the potential value of our portfolio;

•regulatory developments in the United States and foreign countries;

•the impact of laws and regulations;

•our estimates regarding expenses, future revenue, capital requirements and needs for additional financing;

•our financial performance;

•the effect of COVID-19 on the foregoing; and

•other factors detailed under the section entitled “Risk Factors”.

The forward-looking statements contained in this prospectus are based on current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the section entitled “Risk Factors”. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Some of these risks and uncertainties may in the future be amplified by the COVID-19 outbreak

and there may be additional risks that we consider immaterial or which are unknown. It is not possible to predict or identify all such risks. We do not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

PROSPECTUS SUMMARY

The following summary highlights information contained in greater details elsewhere in this prospectus. This summary is not complete and does not contain all of the information you should consider in making your investment decision. You should read the entire prospectus carefully before making an investment in our common stock or warrants. You should carefully consider, among other things, our financial statements and related notes and the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

Company Overview

We seek to fulfill the promise of additive manufacturing, also referred to as 3D printing (“AM”), to deliver breakthroughs in performance, cost and lead time in the production of high-value metal parts.

We produce a full-stack hardware and software solution based on our proprietary powder bed fusion (“PBF”) technology, which enables support-free production. Our technology enables the production of highly complex, mission-critical parts that existing AM solutions cannot produce without the need for redesign or additional assembly. Our products give our customers who are in space, aviation, defense, energy and industrial markets the freedom to design and produce metal parts with complex internal features and geometries that had previously been considered impossible for AM. We believe our technology is years ahead of competitors.

Our technology is novel compared to other AM technologies based on its ability to deliver high-value metal parts that have complex internal channels, structures and geometries. This affords a wide breadth of design freedom for creating new metal parts, and it enables replication of existing parts without the need to redesign the part to be manufacturable with AM. Because of these features, we believe our technology and product capabilities are highly valued by our customers. Our customers are primarily original equipment manufacturers (“OEMs”) and contract manufacturers who look to AM to solve issues with traditional metal parts manufacturing technologies. Those traditional manufacturing technologies rely on processes, including casting, stamping, and forging, that typically require high volumes to drive competitive costs and have long lead times for production. Our customers look to AM solutions to produce assemblies that are lighter, stronger and more reliable than those manufactured with traditional technologies. Our customers also expect AM solutions to drive lower costs for low volume parts and substantially shorter lead times. However, many of our customers have found that legacy AM technologies failed to produce the required designs for the high-value metal parts and assemblies that our customers wanted to produce with AM. As a result, other AM solutions often require that parts be redesigned so that they can be produced and frequently incur performance losses for high-value applications. For these reasons, AM solutions of our competitors have been largely relegated to tooling and prototyping or the production of less complex, lower-value metal parts.

In contrast, our technology can deliver complex high-value metal parts with the design advantages, lower costs and faster lead times associated with AM, and generally avoids the need to redesign the parts. As a result, our customers have increasingly adopted our technology into their design and production processes. We believe our value is reflected in our sales patterns, as most customers purchase a single machine to validate our technology and purchase additional systems over time as they embed our technology in their product roadmap and manufacturing infrastructure. We consider this approach a “land and expand” strategy, oriented around a demonstration of our value proposition followed by increasing penetration with key customers.

Our customers range from small- and medium-sized enterprises to Fortune 500 companies in the space, aviation, defense, energy and industrial markets. As of June 30, 2021, December 31, 2020 and December 31, 2019, we had sixteen, eight and three customers, respectively, for our 3D Printer sales, and SpaceX, our largest customer, accounted for approximately, 16.3%, 40.8% and 74.9% of our revenue for the six months ended June 30, 2021 and the fiscal years ended December 31, 2020 and 2019, respectively. Including part sales and other services to customers, we had 66 customers as of June 30, 2021. Our customers include both OEMs, as well as contract manufacturers who provide service and parts on behalf of OEMs.

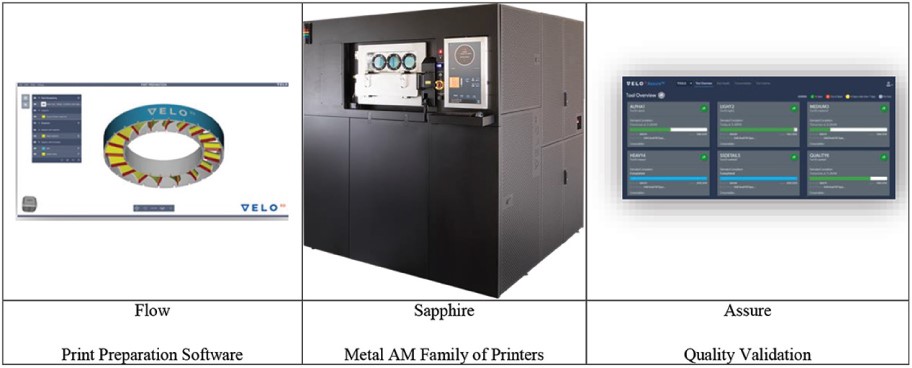

We offer customers a full-stack solution, which includes the following key components:

•Flow™ print preparation software conducts sophisticated analysis of the features of the metal part and specifies a production process that enables support-free printing of the part.

•Sapphire® metal AM printers produce the part using our proprietary PBF technology, which enables support-free production. Our technology produces metal parts by fusing many thousands of very thin layers of metal powder with precisely controlled laser beams in a sophisticated software-defined sequence (or “recipe”) defined by our Flow software.

•Assure™ quality validation software validates the product made by Sapphire to confirm that it is made to the specifications required by the original design.

Legacy AM technologies often rely on internal supports to prevent deformation of the metal part during the 3D printing process. These supports inhibit the production of parts with complex internal geometries, which are often required in high-performance applications, because there is limited or no access to remove them after production. Our technological advances enable our Sapphire product to print metal parts that do not require internal supports, enabling our customers to produce designs that would otherwise be infeasible to make with AM.

We sell our full-stack hardware and software AM solution through two types of transaction models: a 3D printer sale transaction and a recurring payment transaction. 3D printer sale transactions are structured as a payment of a fixed purchase price for the system. Recurring payment transactions fall into two categories: a leased 3D printer transaction and a sale and utilization fee model. Under the leased 3D printer transaction, the customer typically pays an amount for a lease that entitles the customer to a base number of hours of usage. For usage above that level, the customer typically pays an hourly usage fee. Most of our leases have a 12-month term, though in certain cases the lease term is longer. In the sale and utilization fee model, customers pay an up-front amount that is less than the full purchase price to purchase the system. This purchase price is supplemented by an hourly usage fee for each hour of system utilization over the life of the system. We intend to more fully transition our recurring payment transactions to this sale and utilization fee model in 2022 and future years. Support services are included with a 3D printer sale transaction and a recurring payment transaction.

We have seen strong demand for our next generation flagship Sapphire XC product, which we plan to begin shipping by the end of 2021. It is anticipated that this product will be able to make parts that are five times the size of parts made by our existing Sapphire product and will reduce part costs by 65% to 80%. Together, the increase in capabilities and improvement in economics for our customers are anticipated to rapidly increase the potential applications of our technology. As of June 30, 2021, our aggregate backlog of $80.7 million comprised $25.5 million of bookings and $55.2 million of reservations for Sapphire XC systems. Demand for the Sapphire XC product is a significant contributor to our expectation for meaningful sales growth from 2022 and beyond.

Corporate Information

We were incorporated on September 11, 2020 as a special purpose acquisition company and a Cayman Islands exempted company under the name JAWS Spitfire Acquisition Corporation. On December 7, 2020, JAWS Spitfire completed its initial public offering. On July 22, 2021, JAWS Spitfire consummated the Business Combination with Velo3D pursuant to the Business Combination Agreement. In connection with the Business Combination, JAWS Spitfire’s jurisdiction of incorporation was changed from the Cayman Islands to the State of Delaware, and JAWS Spitfire changed its name to Velo3D, Inc.

Our address is 511 Division Street, Campbell, CA 95008. Our telephone number is (408) 610-3915. Our website address is https://www.velo3d.com. Information contained on our website or connected thereto does not constitute part of, and is not incorporated by reference into, this prospectus or the registration statement of which it forms a part.

Summary of Risk Factors

In evaluating an investment in our securities, investors should carefully read the risks described below, this prospectus and especially consider the factors discussed in the section entitled “Risk Factors.” If any of the following events occur, our business, financial condition and operating results may be materially adversely affected. In that event, the trading price of our securities could decline, and you could lose all or part of your investment. Such risks include, but are not limited to:

Risks Related to Our Financial Position and Need for Additional Capital

•We are an early-stage company with a history of losses. We have not been profitable historically and may not achieve or maintain profitability in the future.

•Our limited operating history and rapid growth makes evaluating our current business and future prospects difficult and may increase the risk of your investment.

•We expect to rely on a limited number of customers for a significant portion of our near-term revenue.

•We may require additional capital to support business growth, and this capital might not be available on acceptable terms, if at all.

•We have invested and expect to continue to invest in research and development efforts that further enhance our products. Such investments may affect our operating results and liquidity, and, if the return on these investments is lower or develops more slowly than we expect, our revenue and operating results may suffer.

Risks Related to Our Business and Industry

•We may experience significant delays in the design, production and launch of our additive manufacturing solutions, and we may be unable to successfully commercialize products on our planned timelines.

•As part of our growth strategy, we intend to continue to acquire or make investments in other businesses, patents, technologies, products or services. Our failure to do so successfully could disrupt our business and have an adverse impact on our financial condition.

•Our business activities may be disrupted due to the outbreak of the COVID-19 pandemic.

•Changes in our product mix may impact our gross margins and financial performance.

•Our business model is predicated, in part, on building a customer base that will generate a recurring stream of revenues through the use of our additive manufacturing system and service contracts. If that recurring stream of revenues does not develop as expected, or if our business model changes as the industry evolves, our operating results may be adversely affected.

•If demand for additive manufacturing products does not grow as expected, or if market adoption of additive manufacturing technology does not continue to develop, or develops more slowly than expected, our revenues may stagnate or decline, and our business may be adversely affected.

•If we fail to meet our customers’ price expectations, demand for our products and product lines could be negatively impacted and our business and results of operations could suffer.

•Declines in the prices of our products and services, or in our volume of sales, together with our relatively inflexible cost structure, may adversely affect our financial results.

•Reservations for our Sapphire XC solution may not convert to purchase orders.

•Defects in our additive manufacturing system or in enhancements to our existing additive manufacturing systems that give rise to part failures for our customers, resulting in product liability or warranty or other

claims that could result in material expenses, diversion of management time and attention and damage to our reputation.

•The additive manufacturing industry in which we operate is characterized by rapid technological change, which requires us to continue to develop new products and innovations to meet constantly evolving customer demands and which could adversely affect market adoption of our products.

•The additive manufacturing industry is competitive. We expect to face increasing competition in many aspects of our business, which could cause our operating results to suffer.

•Our existing and planned global operations subject us to a variety of risks and uncertainties that could adversely affect our business and operating results. Our business is subject to risks associated with selling machines and other products in non-United States locations.

•We have identified material weaknesses in our internal control over financial reporting, and we may identify additional material weaknesses in the future or otherwise fail to maintain effective internal control over financial reporting, which may result in material misstatements of our financial statements or cause us to fail to meet our periodic reporting obligations or cause our access to the capital markets to be impaired and have a material adverse effect on our business.

Risks Related to Third Parties

•We could be subject to personal injury, property damage, product liability, warranty and other claims involving allegedly defective products that we supply.

•We may rely heavily on future collaborative and supply chain partners.

•If our suppliers become unavailable or inadequate, our customer relationships, results of operations and financial condition may be adversely affected.

Risks Related to Operations

•We operate primarily at a facility in a single location, and any disruption at this facility could adversely affect our business and operating results.

•Construction of our planned production facilities may not be completed in the expected timeframe or in a cost-effective manner. Any delays in the construction of our production facilities could severely impact our business, financial condition, results of operations and prospects.

•Maintenance, expansion and refurbishment of our facilities, the construction of new facilities and the development and implementation of new manufacturing processes involve significant risks.

Risks Related to Compliance Matters

•We are subject to U.S. and other anti-corruption laws, trade controls, economic sanctions and similar laws and regulations. Our failure to comply with these laws and regulations could subject us to civil, criminal and administrative penalties and harm our reputation.

•We are subject to environmental, health and safety laws and regulations related to our operations and the use of our additive manufacturing systems and consumable materials, which could subject us to compliance costs and/or potential liability in the event of non compliance.

Risks Related to Intellectual Property

•Our business relies on proprietary information and other intellectual property (“IP”), and our failure to protect our IP rights could harm our competitive advantages with respect to the use, manufacturing, sale or other commercialization of our processes, technologies and products, which may have an adverse effect on our results of operations and financial condition.

•Third-party lawsuits and assertions to which we are subject alleging our infringement of patents, trade secrets or other IP rights may have a significant adverse effect on our financial condition.

Emerging Growth Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

Further, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a registration statement under the Securities Act declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. We have elected not to opt out of such extended transition period, which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of our financial statements with certain other public companies difficult or impossible because of the potential differences in accounting standards used.

We will remain an emerging growth company until the earliest of (i) the last day of the fiscal year: (a) following December 7, 2025, the fifth anniversary of the closing of our IPO; (b) in which we have total annual gross revenue of at least $1.07 billion; or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeds $700.0 million as of the last business day of our most recently completed second fiscal quarter; and (ii) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the prior three-year period. References herein to “emerging growth company” have the meaning associated with it in the JOBS Act.

Smaller Reporting Company

Additionally, we are a “smaller reporting company” as defined in Item 10(f)(1) of Regulation S-K. Smaller reporting companies may take advantage of certain reduced disclosure obligations, including, among other things, providing only two years of audited financial statements. We will remain a smaller reporting company until the last day of the fiscal year in which (i) the market value of our common stock held by non affiliates exceeds $250 million as of the prior June 30, or (ii) our annual revenues exceeded $100 million during such completed fiscal year and the market value of our common stock held by non affiliates exceeds $700 million as of the prior June 30.

The Offering

| | | | | |

Issuer | Velo3D, Inc. |

| |

| Issuance of common stock | |

| |

| Shares of common stock offered by us | Up to 13,075,000 shares of common stock issuable upon exercise of warrants, consisting of: a.up to 8,625,000 shares of common stock that are issuable upon the exercise of the public warrants; and b.up to 4,450,000 shares of common stock that are issuable upon the exercise of the private placement warrants |

| |

| Shares of common stock outstanding as of September 29, 2021 | 183,163,826 shares of common stock |

| |

| Exercise price of public warrants and private placement warrants | $11.50 per share, subject to adjustments as described herein |

| |

| Use of proceeds | We will receive up to an aggregate of approximately $150.4 million from the exercise of the warrants, assuming the exercise in full of all of the warrants for cash. We expect to use the net proceeds from the exercise of the warrants for investment in growth and general corporate purposes. See “Use of Proceeds.” |

| |

| Resale of common stock and warrants | |

| |

| Shares of common stock offered by the Selling Securityholders | Up to 169,147,569 shares of common stock, consisting of: a.up to 15,500,000 PIPE Shares; b.up to 8,625,000 Founder Shares; c.up to 140,572,569 shares of common stock issued or issuable to the Velo3D equity holders in connection with or as a result of the consummation of the Business Combination consisting of: (i)up to 123,058,137 shares of our common stock; (ii)up to 1,902,945 shares of common stock issuable upon the exercise of certain options; and (iii)up to 15,611,487 Earn-Out Shares d.up to 4,450,000 shares of our common stock issuable upon the exercise of the private placement warrants |

| |

| Warrants offered by the Selling Securityholders | Up to 4,450,000 private placement warrants |

| |

| Terms of the offering | The Selling Securityholders will determine when and how they will dispose of the shares of common stock and warrants registered under this prospectus for resale. |

| |

| Use of proceeds | We will not receive any proceeds from the sale of shares of common stock or warrants by the Selling Securityholders. |

| |

| | | | | |

| Lock-up restrictions | Certain of our stockholders are subject to certain restrictions on transfer until the termination of applicable lock-up periods. See “Certain Relationships and Related Person Transactions — Related Party Transactions Entered into in Connection with the Business Combination — Amended and Restated Registration Rights Agreement” and “— Lock-Up Agreement with Mr. Buller.” |

| |

NYSE symbols | Our common stock and public warrants are listed on the NYSE under the symbols VLD and VLD WS, respectively. |

| |

Risk factors | See “Risk Factors” and other information included in this prospectus for a discussion of factors you should consider before investing in our securities. |

SELECTED HISTORICAL FINANCIAL INFORMATION OF VELO3D

The selected historical statements of operations data of Velo3D for the six months ended June 30, 2021 and 2020 and the years ended December 31, 2020 and 2019 and the historical balance sheet data as of June 30, 2021 and December 31, 2020 and 2019 are derived from Velo3D’s audited financial statements and unaudited interim financial statements included elsewhere in this prospectus. Velo3D’s historical results are not necessarily indicative of the results that may be expected in the future. You should read the following selected historical financial data together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Velo3D’s financial statements and related notes included elsewhere in this prospectus.

| | | | | | | | | | | | | | | | | | | | | | | |

| (in thousands) | Six months ended

June 30, | | Year ended

December 31, |

| 2021 | | 2020 | | 2020 | | 2019 |

| Revenue | $ | 8,318 | | | $ | 9,960 | | | $ | 18,975 | | | $ | 15,223 | |

| Cost of revenue | 6,524 | | | 6,455 | | | 12,608 | | | 10,393 | |

| Gross profit (loss) | 1,794 | | | 3,505 | | | 6,367 | | | 4,830 | |

| Operating expenses | | | | | | | |

| Research and development | 11,094 | | | 6,874 | | | 14,188 | | | 14,593 | |

| Selling and marketing | 4,360 | | | 2,875 | | | 7,004 | | | 8,600 | |

| General and administrative | 10,004 | | | 4,128 | | | 6,382 | | | 6,929 | |

| Total operating expenses | 25,458 | | | 13,877 | | | 27,574 | | | 30,122 | |

| Loss from operations | (23,664) | | | (10,372) | | | (21,207) | | | (25,292) | |

| Interest expense | (644) | | | (152) | | | (639) | | | (605) | |

| Other income (expense), net | (1,778) | | | 40 | | | 39 | | | 219 | |

| Loss before provision for income taxes | (26,086) | | | (10,484) | | | (21,807) | | | (25,678) | |

| Provision for income taxes | — | | | — | | | — | | | — | |

| Net loss and comprehensive loss | (26,086) | | | (10,484) | | | (21,807) | | | (25,678) | |

Cash and cash equivalents

| | | | | | | | | | | | | | | | | |

| As of

June 30, | | As of

December 31, |

| (in thousands) | 2021 | | 2020 | | 2019 |

| Balance Sheet Data: | | | | | |

| Cash and cash equivalents | $ | 11,948 | | | $ | 15,517 | | | $ | 9,815 | |

| Total assets | 40,233 | | | 32,691 | | | 21,633 | |

| Total debt | 18,883 | | | 8,003 | | | 6,128 | |

| Total liabilities | 48,943 | | | 16,808 | | | 20,598 | |

| Total redeemable convertible preferred stock | 123,704 | | | 123,701 | | | 101,858 | |

| Total stockholders’ deficit | $ | (132,414) | | | $ | (107,821) | | | $ | (100,823) | |

We use non-GAAP financial measures to help us make strategic decisions, establish budgets and operational goals for managing its business, analyze our financial results, and evaluate our performance. We also believe that the presentation of these non-GAAP financial measures in this prospectus provides an additional tool for investors to use in comparing our core business and results of operations over multiple periods. However, the non-GAAP financial measures presented in this prospectus may not be comparable to similarly titled measures reported by other companies due to differences in the way that these measures are calculated. The non-GAAP financial measures presented in this prospectus should not be considered as the sole measure of our performance and should not be considered in isolation from, or as a substitute for, comparable financial measures calculated in accordance with generally accepted accounting principles accepted in the United States (“GAAP”).

The information in the table below sets forth the non-GAAP financial measures that we use in this prospectus. Because of the limitations associated with these non-GAAP financial measures, “EBITDA,” “Adjusted EBITDA” and “Adjusted EBITDA as a percent of revenue” should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA, Adjusted EBITDA and Adjusted EBITDA as a percent of revenue on a supplemental basis. You should review the reconciliation of the non-GAAP financial measures below and not rely on any single financial measure to evaluate our business. Please see “Audited Financial Statements of Velo3D, Inc.” in this prospectus. The definitions for the Non-GAAP financial measures, EBITDA, Adjusted EBITDA and Adjusted EBITDA as a percent of revenue, are described within “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The following table reconciles Net loss to EBITDA and Adjusted EBITDA during the six months ended June 30, 2021 and 2020 and the years ended December 31, 2020 and 2019, respectively:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Six Months Ended June 30, | | Year Ended December 31, |

| 2021 | | 2020 | | 2020 | | 2019 |

| In thousands | | As a percentage of revenue | | In thousands | | As a percentage of revenue | | In thousands | | As a percentage of revenue | | In thousands | | As a percentage of revenue |

| Revenue | $ | 8,318 | | | 100.0 | % | | $ | 9,960 | | | 100.0 | % | | $ | 18,975 | | | 100.0 | % | | $ | 15,223 | | | 100.0 | % |

| Net loss | (26,086) | | | (313.6) | % | | (10,484) | | | (105.3) | % | | (21,807) | | | (114.9) | % | | (25,678) | | | (168.7) | % |

| Interest expense | 644 | | | 7.7 | % | | 152 | | | 1.5 | % | | 639 | | | 3.4 | % | | 605 | | | 4.0 | % |

| Tax expense | — | | | — | % | | — | | | — | % | | — | | | — | % | | — | | | — | % |

| Depreciation and amortization | 692 | | | 8.3 | % | | 529 | | | 5.3 | % | | 1,240 | | | 6.5 | % | | 1,138 | | | 7.5 | % |

| EBITDA | (24,750) | | | (3.0) | % | | (9,803) | | | (98.4) | % | | (19,928) | | | (105.0) | % | | (23,935) | | | (157.2) | % |

| Stock based compensation | 1,075 | | | 12.9 | % | | 777 | | | 7.8 | % | | 1,455 | | | 7.7 | % | | 1,472 | | | 9.7 | % |

| Change in fair value of warrant liabilities | 1,741 | | | 20.9 | % | | (7) | | | (0.1) | % | | (3) | | | — | % | | (5) | | | — | % |

| Adjusted EBITDA | $ | (21,934) | | | (263.7) | % | | $ | (9,033) | | | (90.7) | % | | $ | (18,476) | | | (97.4) | % | | $ | (22,468) | | | (147.6) | % |

SELECTED HISTORICAL FINANCIAL INFORMATION OF JAWS SPITFIRE

The selected historical financial data as of December 31, 2020, and for the period from September 11, 2020 (inception) through December 31, 2020, are derived from JAWS Spitfire’s audited financial statements included elsewhere in this prospectus. The selected historical interim financial data as of June 30, 2021 and for the six months ended June 30, 2021 are derived from JAWS Spitfire’s unaudited interim financial statements included elsewhere in this prospectus.

JAWS Spitfire’s historical results are not necessarily indicative of future results, and the results for any interim period are not necessarily indicative of the results that may be expected for a full fiscal year.

| | | | | | | | | | | |

| For the Six Months Ended June 30, 2021 | | Period from September 11, 2020 (inception) through December 31, 2020 |

| | | As Restated |

| Statement of Operations Data | | | |

| General and administrative expenses | $ | 4,629,818 | | | $ | 183,573 | |

| Transaction costs | — | | | 1,583,878 | |

Loss from operations | (4,629,818) | | | (1,767,451) | |

| Other Income | | | |

| Change in fair value of warrant liabilities | 18,043,500 | | | — | |

| Interest earned on marketable securities held in Trust Account | 9,910 | | | — | |

Net Income | 13,423,592 | | | — | |

| Weighted average shares outstanding of Class A redeemable ordinary shares | 34,500,000 | | | 34,500,000 | |

Basic and diluted net income per share, Class A | $ | — | | | $ | — | |

| Weighted average shares outstanding of Class B non-redeemable ordinary shares | 8,625,000 | | | 7,758,028 | |

Basic and diluted net income (loss) per share, Class B | $ | 1.56 | | | $ | (0.23) | |

| | | | | | | | | | | |

| June 30, 2021 | | December 31, 2020 |

| | | As Restated |

| Condensed Balance Sheet Data (At Period End): | | | |

| Total assets | $ | 345,529,674 | | | $ | 347,394,817 | |

| Total liabilites | $ | 40,638,405 | | | $ | 55,927,140 | |

| Class A ordinary shares, $0.0001 par value; 200,000,000 shares authorized; 4,510,874 and 5,853,233 shares issued and outstanding (excluding 29,989,126 and 28,646,767 shares subject to possible redemption) at June 30, 2021 and December 31, 2020, respectively | 451 | | | 585 | |

| Class B ordinary shares, $0.0001 par value; 20,000,000 shares authorized; 8,625,000 shares issued and outstanding at June 30, 2021 and December 31, 2020 | 863 | | | 863 | |

| Total shareholders’ equity | $ | 5,000,009 | | | $ | 5,000,007 | |

RISK FACTORS

Investing in our securities involves risks. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, before deciding whether to purchase any of our securities. Our business, results of operations, financial condition, and prospects could also be harmed by risks and uncertainties that are not presently known to us or that we currently believe are not material. If any of these risks actually occur, our business, results of operations, financial condition, and prospects could be materially and adversely affected. Unless otherwise indicated, references in these risk factors to our business being harmed will include harm to our business, reputation, brand, financial condition, results of operations, and prospects. In such event, the market price of our securities could decline, and you could lose all or part of your investment.

Risks Related to Our Business

Risks Related to Our Financial Position and Need for Additional Capital

We are an early-stage company with a history of losses. We have not been profitable historically and may not achieve or maintain profitability in the future.

We experienced net losses in each year from our inception, including net losses of $21.8 million and $25.7 million for the years ended December 31, 2020 and 2019, respectively. We believe we will continue to incur operating losses and negative cash flow in the near-term as we continue to invest significantly in our business, in particular across our research and development (“R&D”) efforts and sales and marketing programs. These investments may not result in increased revenue or growth in our business.

As a public company, we incur significant additional legal, accounting and other expenses that Velo3D did not incur as a private company. These increased expenditures may make it harder for us to achieve and maintain future profitability. Revenue growth and growth in our customer base may not be sustainable, and we may not achieve sufficient revenue to achieve or maintain profitability. While we have generated revenue in the past, we have only recently begun commercial shipments of several of our announced additive manufacturing solutions, some of which are expected to generate a substantial portion of our revenue going forward, and it is difficult for us to predict our future operating results. We may incur significant losses in the future for a number of reasons, including due to the other risks described in this prospectus, and we may encounter unforeseen expenses, difficulties, complications and delays and other unknown events. As a result, our losses may be larger than anticipated, we may incur significant losses for the foreseeable future, and we may not achieve profitability when expected, or at all, and even if we do, we may not be able to maintain or increase profitability. Furthermore, if our future growth and operating performance fail to meet investor or analyst expectations, or if we have future negative cash flow or losses resulting from our investment in acquiring customers or expanding our operations, this could make it difficult for you to evaluate our current business and our future prospects and have a material adverse effect on our business, financial condition and results of operations.

Our limited operating history and rapid growth makes evaluating our current business and future prospects difficult and may increase the risk of your investment.

Much of our growth has occurred in recent periods. Our limited operating history may make it difficult for you to evaluate our current business and our future prospects, as we continue to grow our business. Our ability to forecast our future operating results is subject to a number of uncertainties, including our ability to plan for and model future growth. We have encountered, and will continue to encounter, risks and uncertainties frequently experienced by growing companies in rapidly evolving industries as we continue to grow our business. If our assumptions regarding these uncertainties, which we use to plan our business, are incorrect or change in reaction to changes in our markets, or if we do not address these risks successfully, our operating and financial results could differ materially from our expectations, our business could suffer, and the trading price of our securities may decline. In addition to our revenue model based on product sales, we are also focused on an annual recurring payment transaction model. This transition may affect our revenue levels in the near term. There are no assurances

that we will be able to secure future business with customers or that such our recurring revenue model will be successful our planned timelines or at all.

It is difficult to predict our future revenues and appropriately budget for our expenses, and we have limited insight into trends that may emerge and affect our business. If actual results differ from our estimates or we adjust our estimates in future periods, our operating results and financial position could be materially affected.

We expect to rely on a limited number of customers for a significant portion of our near-term revenue.

We currently have purchase orders with a limited number of customers, from which we expect to generate most of our revenues in the near future. Approximately 16.3%, 40.8% and 74.9% of our revenue was derived from sales through a single customer, SpaceX, for the six months ended June 30, 2021 and the fiscal years ended December 31, 2020 and 2019, respectively, and we anticipate that a significant portion of our revenue will continue to be derived from sales through this customer in the foreseeable future. We had sixteen and eight customers in total as of June 30, 2021 and December 31, 2020 for our 3D Printer sales. Including part sales and other services to customers, we had 66 and 42 customers as of June 30, 2021 and December 31, 2020, respectively. Our 3D printer sales occur under purchase orders that are governed by our terms and conditions of sale. The Company’s terms and conditions with SpaceX are consistent with all other customers and permit the customer to terminate the Company’s services at any time (subject to notice and certain other provisions). Accordingly, the sudden loss of SpaceX or one or more of our other significant customers, the renegotiation of a significant customer contract, a substantial reduction in their orders, their failure to exercise customer options, their unwillingness to extend contractual deadlines if we are unable to meet production requirements, their inability to perform under their contracts or a significant deterioration in their financial condition could harm our business, results of operations and financial condition. If we fail to perform under the terms of these agreements, the customers could seek to terminate these agreements and/or pursue damages against us, including liquidated damages in certain instances, which could harm our business.

Because we rely on a limited number of customers for a significant portion of our revenues, we depend on the creditworthiness of these customers. If the financial condition of our customers declines, our credit risk could increase. Should one or more of our significant customers declare bankruptcy, be declared insolvent or otherwise be restricted by state or federal laws or regulation from continuing in some or all of their operations, this could adversely affect our ongoing revenues, the collectability of our accounts receivable and our net income.

We may require additional capital to support business growth, and this capital might not be available on acceptable terms, if at all.

We intend to continue to make investments to support our business growth and may require additional funds to respond to business challenges and opportunities, including the need to develop new features or enhance our products, expand our manufacturing capacity, improve our operating infrastructure or acquire complementary businesses and technologies. Accordingly, we may need to engage in equity or debt financings to secure additional funds if our existing sources of cash and any funds generated from operations do not provide us with sufficient capital. If we raise additional funds through future issuances of equity or convertible debt securities, our existing stockholders could suffer significant dilution, and any new equity securities we issue could have rights, preferences and privileges superior to those of holders of our common stock. Any debt financing that we may secure in the future could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities, including potential acquisitions. We may not be able to obtain additional financing on terms favorable to us, if at all. If we are unable to obtain adequate financing or financing on terms satisfactory to us when we require it, our ability to continue to support our business growth and to respond to business challenges and opportunities could be significantly impaired, and our business may be adversely affected.

We have invested and expect to continue to invest in research and development efforts that further enhance our products. Such investments may affect our operating results and liquidity, and, if the return on these investments is lower or develops more slowly than we expect, our revenue and operating results may suffer.

We have invested and expect to continue to invest in research and development efforts that further enhance our products. These investments may involve significant time, risks and uncertainties, including the risk that the expenses associated with these investments may affect our margins, operating results and liquidity and that such investments may not generate sufficient revenues to offset liabilities assumed and expenses associated with these new investments. The AM industry changes rapidly as a result of technological and product developments, which may render our solutions less effective. We believe that we must continue to invest a significant amount of time and resources in our products to maintain and improve our competitive position. If we do not achieve the benefits anticipated from these investments, if the achievement of these benefits is delayed, our business, operating results and prospects may be materially adversely affected.

Risks Related to Our Business and Industry

We may experience significant delays in the design, production and launch of our additive manufacturing solutions, and we may be unable to successfully commercialize products on our planned timelines.

There are significant technological and logistical challenges associated with producing, marketing, selling and delivering additive manufacturing systems such as ours that make high-value component parts for customers, and we may not be able to resolve all of the difficulties that may arise in a timely or cost-effective manner, or at all. While we believe that we understand the engineering and process characteristics necessary to successfully design and produce additive manufacturing systems to make high-value metal parts for our customers, our assumptions may prove to be incorrect, and we may be unable to consistently produce additive manufacturing products in an economical manner in commercial quantities.

Certain additive manufacturing solutions are still under development. There are often delays in the design, testing, manufacture and commercial release of new products, and any delay in the launch of our products could materially damage our brand, business, growth prospects, financial condition and operating results. Even if we successfully complete the design, testing and manufacture for one or all of our products under development, we may fail to develop a commercially successful product on the timeline we expect for a number of reasons, including:

•misalignment between the products and customer needs;

•lack of innovation of the product;

•failure of the product to perform in accordance with the customer’s industry standards;

•ineffective distribution and marketing;

•delay in obtaining any required regulatory approvals;

•unexpected production costs; or

•release of competitive products.

Our success in the market for the products we develop will depend largely on our ability to prove our products’ capabilities in a timely manner. Upon demonstration, our customers may not believe that our products and/or technology have the capabilities they were designed to have or that we believe they have. Furthermore, even if we do successfully demonstrate our products’ capabilities, potential customers may be more comfortable doing business with another larger and more established company or may take longer than expected to make the decision to order our products. Significant revenue from new product investments may not be achieved for a number of years, if at all. If the timing of our launch of new products and/or of our customers’ acceptance of such products is different than our assumptions, our revenue and results of operations may be adversely affected.

Additionally, we are in the process of establishing a recurring payment offering for customers, which may present similar challenges to those outlined above with respect to the design, production and launch of new additive manufacturing solutions. In particular, we may fail to develop a commercially successful offering if we are unable to meet customer needs or industry standards, if we fail to meet customer price expectations or if our marketing and distribution strategy proves ineffective. If we are unable to establish such an offering, sales of our additive manufacturing solutions and our overall operating results could suffer.

As part of our growth strategy, we intend to continue to acquire or make investments in other businesses, patents, technologies, products or services. Our failure to do so successfully could disrupt our business and have an adverse impact on our financial condition.

As part of our business strategy, we have entered into, and expect to enter into, agreements to acquire or invest in other companies. To the extent we seek to grow our business through acquisitions, we may not be able to successfully identify attractive acquisition opportunities or consummate any such acquisitions if we cannot reach an agreement on commercially favorable terms, if we lack sufficient resources to finance the transaction on our own and cannot obtain financing at a reasonable cost or if regulatory authorities prevent such transaction from being consummated. In addition, competition for acquisitions in the markets in which we operate during recent years has increased, and may continue to increase, which may result in an increase in the costs of acquisitions or cause us to refrain from making certain acquisitions. We may not be able to complete future acquisitions on favorable terms, if at all.

If we do complete future acquisitions, we cannot assure you that they will ultimately strengthen our competitive position or that they will be viewed positively by customers, financial markets or investors. Furthermore, future acquisitions could pose numerous additional risks to our operations, including:

•diversion of management’s attention from their day-to-day responsibilities;

•unanticipated costs or liabilities associated with the acquisition;

•increases in our expenses;

•problems integrating the purchased business, products or technologies;

•challenges in achieving strategic objectives, cost savings and other anticipated benefits;

•inability to maintain relationships with key customers, suppliers, vendors and other third parties on which the purchased business relies;

•the difficulty of incorporating acquired technology and rights into our platform and of maintaining quality and security standards consistent with our brand;

•difficulty in maintaining controls, procedures and policies during the transition and integration;

•challenges in integrating the new workforce and the potential loss of key employees, particularly those of the acquired business; and

•use of substantial portions of our available cash or the incurrence of debt to consummate the acquisition.

If we proceed with a particular acquisition, we may have to use cash, issue new equity securities with dilutive effects on existing stockholders, incur indebtedness, assume contingent liabilities or amortize assets or expenses in a manner that might have a material adverse effect on our financial condition and results of operations. Acquisitions will also require us to record certain acquisition-related costs and other items as current period expenses, which would have the effect of reducing our reported earnings in the period in which an acquisition is consummated. In addition, we could also face unknown liabilities or write-offs due to our acquisitions, which could result in a significant charge to our earnings in the period in which they occur. We will also be required to record goodwill or other long-lived asset impairment charges (if any) in the periods in which they occur, which could result in a significant charge to our earnings in any such period.

Achieving the expected returns and synergies from future acquisitions will depend, in part, upon our ability to integrate the products and services, technology, administrative functions and personnel of these businesses into our product lines in an efficient and effective manner. We cannot assure you that we will be able to do so, that our acquired businesses will perform at levels and on the timelines anticipated by our management or that we will be able to obtain these synergies. In addition, acquired technologies and IP may be rendered obsolete or uneconomical by our own or our competitors’ technological advances. Management resources may also be diverted from operating our existing businesses to certain acquisition integration challenges. If we are unable to successfully integrate acquired businesses, our anticipated revenues and profits may be lower. Our profit margins may also be lower, or diluted, following the acquisition of companies whose profit margins are less than those of our existing businesses.

Our business activities may be disrupted due to the outbreak of the COVID-19 pandemic.

We face various risks and uncertainties related to the global outbreak of COVID-19. In recent months, the continued spread of COVID-19, including variant strains of the virus, has led to disruption and volatility in the global economy and capital markets, which has increased the cost of capital and adversely impacted access to capital. Government-enforced travel bans and business closures around the world have significantly impacted our ability to sell, install and service our additive manufacturing systems at customers around the world. It has, and may continue to, disrupt our third-party contract manufacturers and supply chain, and our ability to perform the final assembly and testing of our systems. We may expect some delays in installation of our products at customers’ facilities, which could lead to postponed customer acceptance of the transactions. Furthermore, if significant portions of our workforce are unable to work effectively, including because of illness, quarantines, government actions, facility closures, remote working or other restrictions in connection with the COVID-19 pandemic, our operations will likely be adversely impacted.

It is not currently possible to reliably project the direct impact of COVID-19 on our operating revenues and expenses. If the COVID-19 pandemic continues for a prolonged duration, we or our customers may be unable to perform fully on our contracts, which will likely result in increases in costs and reduction in revenue. These cost increases may not be fully recoverable or adequately covered by insurance. The long-term effects of COVID-19 to the global economy and to us are difficult to assess or predict and may include a decline in the market prices of our products, risks to employee health and safety, risks for the deployment of our products and services and reduced sales in impacted geographic locations. Any prolonged restrictive measures put in place in order to control COVID-19 or other adverse public health developments in any of our targeted markets may have a material and adverse effect on our business operations and results of operations.

To the extent the COVID-19 pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section, including but not limited to those relating to cyber-attacks and security vulnerabilities, interruptions or delays due to third parties or our ability to raise additional capital or generate sufficient cash flows necessary to fulfill our obligations under our existing indebtedness or to expand our operations.

Changes in our product mix may impact our gross margins and financial performance.

Our financial performance may be affected by the mix of transaction models under which we sell during a given period. Different transaction models have different margins in the period in which the transaction occurs and in subsequent periods. Therefore our gross margins may fluctuate based on the mix of sale and recurring payment transactions in a given period. If our product mix shifts too far into lower gross margin transactions in a given period and we are not able to sufficiently reduce the engineering, production and other costs associated with those transactions or substantially increase the sales of our higher gross margin transactions, our profitability could be reduced. Additionally, the introduction of new products or services may further heighten quarterly fluctuations in gross profit and gross profit margins due to manufacturing ramp-up and start-up costs. We may experience significant quarterly fluctuations in gross profit margins or operating income or loss due to the impact of the mix of products, channels or geographic areas in which we sell our products from period to period.

Our business model is predicated, in part, on building a customer base that will generate a recurring stream of revenues through the use of our additive manufacturing system and service contracts. If that recurring stream of revenues does not develop as expected, or if our business model changes as the industry evolves, our operating results may be adversely affected.

Our business model is dependent, in part, on our ability to maintain and increase sales of our additive manufacturing products and service contracts as they generate recurring revenues. Existing and future customers of our systems may not purchase our products or related service contracts at the same rate at which customers currently purchase those products and services.

If demand for additive manufacturing products does not grow as expected, or if market adoption of additive manufacturing technology does not continue to develop, or develops more slowly than expected, our revenues may stagnate or decline, and our business may be adversely affected.

The industrial manufacturing market, which today is dominated by conventional manufacturing processes that do not involve 3D printing technology, is undergoing a shift towards additive manufacturing. We may not be able to develop effective strategies to raise awareness among potential customers of the benefits of additive manufacturing technologies or our products may not address the specific needs or provide the level of functionality required by potential customers to encourage the continuation of this shift towards additive manufacturing. If additive manufacturing technology does not continue to gain broader market acceptance as an alternative to conventional manufacturing processes, particularly with regard to high value parts, or if the marketplace adopts additive manufacturing technologies that differ from our technologies, we may not be able to increase or sustain the level of sales of our products, and our operating results would be adversely affected as a result.

If we fail to meet our customers’ price expectations, demand for our products and product lines could be negatively impacted and our business and results of operations could suffer.

Demand for our product lines is sensitive to price. We believe our competitive pricing has been an important factor in our results to date. Therefore, changes in our pricing strategies can have a significant impact on our business and ability to generate revenue. Many factors, including our production and personnel costs and our competitors’ pricing and marketing strategies, can significantly impact our pricing strategies. If we fail to meet our customers’ price expectations in any given period, demand for our products and product lines could be negatively impacted and our business and results of operations could suffer.

We use, and plan to continue using, different pricing models for different products. For example, we plan to use a recurring payment pricing model for certain customers. This pricing model is still relatively new to some of our customers and may not be attractive to them, especially in regions where the model is less common. If customers resist this or any other new pricing models we introduce, our revenue may be adversely affected, and we may need to restructure the way in which we charge customers for our products. To date, while we have accepted pre-orders for our Sapphire XC solution. annual subscription pricing, we have not recognized material revenue from these orders, or associated with our recurring payment model in general.

Declines in the prices of our products and services, or in our volume of sales, together with our relatively inflexible cost structure, may adversely affect our financial results.

Our business is subject to price competition. Such price competition may adversely affect our results of operation, especially during periods of decreased demand. Decreased demand also adversely impacts the volume of our additive manufacturing systems sales. If our business is not able to offset price reductions resulting from these pressures, or decreased volume of sales due to contractions in the market, by improved operating efficiencies and reduced expenditures, then our operating results will be adversely affected.

Certain of our operating costs are fixed and cannot readily be reduced, which diminishes the positive impact of our restructuring programs on our operating results. To the extent the demand for our products slows, or the additive manufacturing market contracts, we may be faced with excess manufacturing capacity and related costs that cannot readily be reduced, which will adversely impact our financial condition and results of operations.

Reservations for our Sapphire XC solution may not convert to purchase orders.